See if you can figure out why [Krugman will not like these figures]:

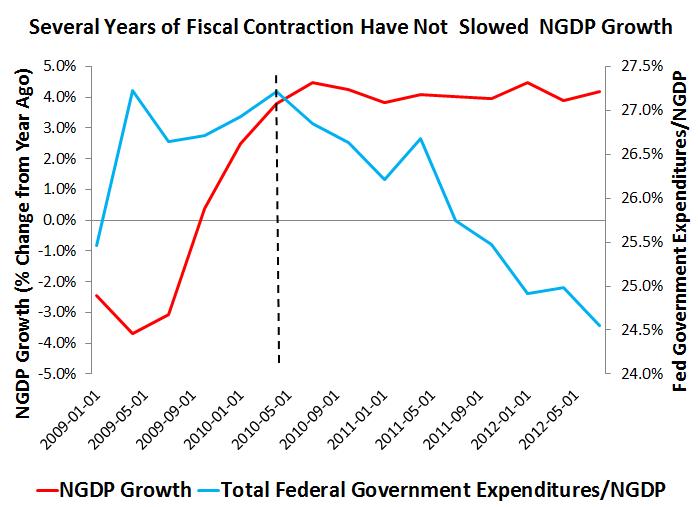

This first figure shows that aggregate demand growth has not been affected by a tightening of fiscal policy since 2010. Specifically, it shows that nominal GDP (NGDP) growth has been remarkably stable since about mid-2010 despite a contraction in federal government expenditures. The same story emerges if we look at the budget deficit relative to NGDP growth:

Both figures seriously undermine the argument for coutercyclical fiscal policy and suggest a very a low fiscal multiplier. They also indicate that the Fed has been doing a remarkable job keeping NGDP growth stable around 4.5%. Monetary policy, in other words, appears to be dominating fiscal policy in terms of stabilizing aggregate demand growth.

Beckworth's conclusion is not necessarily valid, and illustrates the danger in drawing conclusions about structural variables from looking at correlations between macroeconomic aggregates. Here's why the conclusion might not be valid:

Suppose that Keynesian demand management policy works perfectly: in other words, fiscal stimulus perfectly smooths fluctuations in aggregate demand. In that case, you will observe substantial swings in fiscal policy, but no swings whatsoever in aggregate demand. When external shocks push AD up, fiscal tightening will push it back down; when external shocks push AD down, fiscal policy will push it back up.

Beckworth's graphs give no measure of external shocks; hence, they are perfectly consistent with the idea that fiscal stimulus was allowed to wind down as the economy naturally recovered. (Tyler points this out.)

Check out Nick Rowe for an exploration of this idea in much greater depth. Using these graphs to conclude that fiscal policy is ineffective is like saying "Hey, no matter how much power my neighbor's heating system puts out from day to day, his room stays the same temperature; his heater must be useless!" It might be true. Or it might be the exact opposite of true.

Also, note that if fiscal policy is effective (i.e. if the multiplier is high), then aggregate demand will depend not just on current deficits but on expectations of the response of deficits to future external AD shocks. This is a central tenet of the "market monetarism" that Beckworth espouses, but there's no reason that forward-looking expectations can't be applied to fiscal policy as well as monetary policy.

To conclude: The graphs Beckworth shows are perfectly consistent with a large fiscal multiplier. In fact, they are perfectly consistent with the hypothesis that monetary policy is essentially ineffective, that the Fed is basically powerless, and that fiscal policy is capable of doing a perfect job of smoothing NGDP growth all on its own.

Now, I'm not saying Beckworth is wrong, and that the multiplier is big. I'm saying that the graphs he shows do not tell us much about the size of the multiplier. We should always beware of drawing conclusions about structural variables from looking at correlations between macroeconomic aggregates.

Update: David Beckworth responds (in the comments, and in an update to his post):

Noah, the thermostat assumes policy can respond in real time to the shocks. Do you really think fiscal policy is nimble enough to do this? It is reasonable to claim monetary policy can given its flexibility, but it's a stretch with fiscal policy (unless there are large automatic stabilizers built into place).Well, it's possible that there just weren't any big shocks in recent years...stimulus might have just calmly would down as planned, while the economy slowly recovered as expected. Also, remember expectations. Expectations are certainly nimble enough to respond quickly to any shock.

A bigger problem with your alternative story is that it doesn't fit the facts. Fiscal policy has been tightening despite the spate of negative economic shocks over the past few years: Eurozone crisis, debt cliff talks 2011, China slowdown which have kept U.S. economy from having a robust recovery.Well, these are certainly putative negative shocks. They seem like things that might have been shocks. But do we know that they really were shocks? The Eurozone crisis was resolved, the debt cliff talks resulted in compromise, and China's slowdown was not really that big of a deal. Maybe in reality this was small potatoes compared to the basic restorative forces, pushing us to a slow but steady recovery after the Great Recession.

Paul Krugman has made this abundantly clear in many pieces where he repeatedly laments the lack of adequate fiscal policy. Surely he wouldn't be saying this is he thought along the lines of your thermostat example?Ah, but what does Krugman consider a satisfactory outcome? The "recovery" from the Great Recession has seen pre-crisis RGDP (and NGDP) growth rates restored, but at a lower level than the pre-crisis trend; Krugman might just be dissatisfied with this outcome, even if it was the outcome produced by fiscal policy. Remember, Krugman doesn't set fiscal policy, he just talks about it a lot.

I continue to conclude that the notion that fiscal policy is ineffective is not supported by these graphs.

Update 2: Scott Sumner weighs in:

I was asked to comment on Noah Smith’s recent critique of David Beckworth’s post on the fiscal multiplier. I basically agree with Noah, and would simply add that his arguments also suggests that the standard arguments in favor of the effectiveness of fiscal stimulus are also mostly flawed, in basically the same way that he claims Beckworth’s arguments are flawed (ignoring expectations channels, etc.) When it comes to fiscal stimulus it’s all about faith—the data tell us almost nothing.The whole world seems to be converging on the idea that macro data doesn't really reveal the true workings of the macroeconomy...I personally think we can do much better, data-wise, than some simple graphs of macroeconomic aggregates, but it is true that any empirical study of the fiscal multiplier (or the money multiplier, or any such policy effect) is going to have to rely on a theoretical model which itself can't easily be verified with data...

Update 3: This blogger put up some similar graphs comparing monetary aggregates and NGDP. Guess what? Monetary aggregates jump all over the place, NGDP just sails along. Exactly like deficits and NGDP in Beckworth's graphs. There's a lesson here...

Update 4: Paul Krugman weighs in, agreeing about the graphs in question, but saying that I'm too "nihilistic" about how much we can learn from macro data. But this, dear readers, is a topic for another post...

anyway, so short period does not prove any ring.

ReplyDeleteFair points, but doesn't Krugman "draw conclusions about structural variables from looking at correlations between macroeconomic aggregates" when he argues about the effectiveness of fiscal stimulus in posts like this:

ReplyDeletehttp://krugman.blogs.nytimes.com/2012/02/19/wars-and-growth/

It seems like this kind of (weak) argument is very common in the macroeconoblogosphere.

I think the Krugman case is different. First off, to miguel's point, PK's data set is 30+ years, as opposed to DB's 2+ years. Second, PK has a theory, then goes to get the data to check against it - sort of like the scientific method. DB seems to have observed a short-term phenomenon, then constructed a sweeping ad hoc idea that supports a pre-conceived notion that looks to me to be political rather than economic. I'm not sure if this is putting too fine a point on it, but I think not.

DeleteThere's also the A precedes B, therefore A causes (or in this case, anti-causes) B problem. A short data view will be especially prone to this potential fallacy.

I've mentioned to DB in the past the hazard of drawing big conclusions from small data sets, but it seems to be a lesson he is willing to learn.

Cheers!

JzB

That Krugman statistical work was indeed poorly done, as the comments point out at http://krugman.blogs.nytimes.com/2012/02/19/wars-and-growth/

DeleteStill - Noah was able to provide an absolutely contrary scenario that is consistent with the data. Did anyone do that with PK's graph?

DeleteJzB

Ray Lopez -

DeleteOK, I read the comments stream, and it the usual anti-Kenyes, anti-PK carping that got me to stop reading the comment stream there in the first place.

I suggest you have a look at comments by walerrhett [in particular at 5:19 on 2/19/12],and Robert Waldmann.

And why did Sam have to go back 10 months to find a post to criticize? PK posts several times every week.

JzB

@ Jazzbumpa

DeleteDB is not making the logical error you claim he is making. He is not "observ[ing] a short-term phenomenon, then construct[ing] a sweeping ad hoc idea that supports a pre-conceived notion" as you put it. Rather, he is rebutting the mantra that occurs in many, many Krugman posts, namely that "contractionary fiscal policy is contractionary"

Krugman is the one that has claimed that at the ZLB that fiscal austerity is contractionary because it can't or won't get offset by monetary authorities. You can diagram the logical assertion as A --> B (if [fiscal contraction at ZLB] --> [economic contraction]).

What logically follows from that is ~B --> ~A. (if [no economic contraction] --> [no fiscal contraction at ZLB]). That is to say, if you can identify an instance of a country experiencing *normal* economic growth (whatever that means) that has imposed contractionary fiscal policy at the zero lower bound, you have falsified Krugman's hypothesis. That is what Beckworth has done here.

Although DB's logic is sound here, the caveat is that we don't know what *normal* economic growth would have been for the US absent that fiscal consolidation. I take the view that because the US has averaged ~4.5% NGDP growth for the last several decades that you could confidently categorize the last few years of growth as *normal*. But it's possible to argue that the flat red line in the graph is actually a huge failure attributable to fiscal contraction. That's probably what Krugman would argue.

Did you happen to read Noah's post?

DeleteThe alleged rebuttal is a non-starter.

This is the comment I was thinking of (and others like it): "Brian Bailey Toscana, Italia

DeleteUh... This graph from my grad school days make me very suspicious of the 'clearly' obvious determanative value. Got a link to the Rsquared and T values of the coefficient or is this "back of the envelope" econometrics? I luv ya man, but this dog won't hunt without some more statistical work. Feb. 21, 2012 at 3:19 a.m." The correlation is possibly spurious.

@ Jazzbumpa

DeleteYes, I did read Noah's post. I'm no economist, so I'm probably either wrong or not explaining myself clearly.

I don't disagree with Noah's basic argument that, on its own, the comparison of changing govt expenditures with NDGP growth does not conclusively prove the (in)effectiveness of fiscal policy. But, to my mind the data do disprove other people's stories about the effect of fiscal stimulus/austerity on the economy.

For two years now Krugman has been claiming that we need fiscal stimulus now now now or else EUROPE! Double dip recession!

Here's one example from 2010 about Krugman's hypothesis:

Suppose you slash spending equal to 1 percent of GDP... if you do it in the face of an economy up against the zero bound, so that the Fed can’t offset the demand effects with lower rates, it’s going to shrink the economy.

http://krugman.blogs.nytimes.com/2010/07/07/self-defeating-austerity/

Krugman uses an extreme example here, but his basic idea is that when you're at the ZLB, fiscal contraction will lead to economic contraction.

But, if you look at the data, US growth has actually been doing pretty well notwithstanding our steady fiscal austerity. Krugman himself, in advance of the election, pointed out that the US economy was actually recovering pretty well, especially if you buy the "financial crisis recessions are always worse" argument that Reinhart & Rogoff have been making.

Unless you buy Noah's obviously absurd expectations story (that the market has so much confidence in future actions of congress that it has priced in future fiscal stabilization policy), the most reasonable interpretation of this data is Beckworth's - that despite the warnings of Keynesians, monetary authorities CAN offset the effect of contractionary fiscal policy, even at the ZLB.

@Sam

Delete"But, if you look at the data, US growth has actually been doing pretty well notwithstanding our steady fiscal austerity."

Pretty well? According to what standards? Usually NGDP grows faster than trend during a recovery, not slower like it has been.

"despite the warnings of Keynesians, monetary authorities CAN offset the effect of contractionary fiscal policy, even at the ZLB."

How exactly? With which policy? For example Steve Williamson, clearly a non Keynesian, is highly sceptical about the effectiveness of the tools the Fed has been employing. Here is more. (http://newmonetarism.blogspot.com/2012/06/more-on-unconventional-open-market.html)

CA makes good points.

DeleteI brought the data from this graph into an Excel spread sheet, and put best fit straight lines through the relatively straight, non-recessionary years of the 90's, naughts, and 10's. Clearly, the current recovery is at a much lower slope.

http://research.stlouisfed.org/fredgraph.png?g=dtC

The other think Krugman has argued form the very beginning is that the stimulus was too little and the portion going to tax cuts was wasted effort.

@Sam

Delete"For two years now Krugman has been claiming that we need fiscal stimulus now now now or else EUROPE! Double dip recession!"

Sorry, but that isn't what Krugman has been claiming for two years. He's been claiming that without more fiscal stimulus will will not recover the lost ground ("output gap") and will have to be satisfied with high unemployment while growing at nearly the previous rate. He's also be claiming that if we enact fiscal austerity we will have EUROPE! Double dip recession!

Google site:krugman.blogs.nytimes.com "output gap"

to see Krugman's actual position on the need for additional fiscal stimulus. He has repeatedly made the point that merely restoring the previous rate of growth is the problem. To really exit the recession, you need to restore GDP to what it would be if the recession had not occurred. Otherwise, you have to accept a permanently larger unemployment figure as the actual GDP line is parallel, but lower, than the pre-recession trend line.

Here's a representative Krugman post from 2009 about why merely ending the recession via stimulus wasn't enough: you really need to close the output gap.

Deletehttp://krugman.blogs.nytimes.com/2009/08/24/picturing-purgatory/

Krugman mostly predicted the end of stimulus would NOT result in a double dip, was worried that he might be wrong about that.

http://krugman.blogs.nytimes.com/2009/12/01/double-dip-warning/

By 2010, Krugman was all about the jobless recovery/output gap that echoes his first post above:

http://krugman.blogs.nytimes.com/2010/01/08/payrolls-and-paradigms/

Come on, this is amateur manipulation. You got to have SVARs to say stupid things convincingly.

ReplyDeleteI was pretty pissed of today about some slides making a similar point about multipliers in crisis in Bulgaria. The country has a currency board against the euro, had seen a some FDI outflow during the crisis, a construction bust and a bit of austerity.

You got to have SVARs to say stupid things convincingly.

DeleteBuahahahahaha

I cringed at that assertion too.

ReplyDeleteYes, Virginia, there is an endogeneity.

ReplyDeleteAll federal spending is not the same. The stimulative effects of buying gasoline at $200/gallon for Iraqi military operations is much lower than the stimulative effect of grants to battery or rail car manufacturers. It's very odd that so many "liberal" economists refuse to consider this factor now.

ReplyDeleteNoah, the thermostat assumes policy can respond in real time to the shocks. Do you really think fiscal policy is nimble enough to do this? It is reasonable to claim monetary policy can given its flexibility, but it's a stretch with fiscal policy (unless there are large automatic stabilizers built into place).

ReplyDeleteA bigger problem with your alternative story is that it doesn't fit the facts. Fiscal policy has been tightening despite the spate of negative economic shocks over the past few years: Eurozone crisis, debt cliff talks 2011, China slowdown which have kept U.S. economy from having a robust recovery. Paul Krugman has made this abundantly clear in many pieces where he repeatedly laments the lack of adequate fiscal policy. Surely he wouldn't be saying this is he thought along the lines of your thermostat example?

See reply above...

DeleteDon't a lot of fiscal policy responses occur automatically? e.g. when the government stops sending people income, their taxes go down - sometimes even their tax rate - without any additional legislative action required. And when people lose private sector income, various kinds of fiscal support systems kick into action, again without any additional legislation required, or with only simple actions like extending the unemployment benefits.

DeleteAlso, if we have been able to sustain nominal spending growth rates at 4.5% despite unemployment levels between 8% and 9%, then I would say 4.5% is a vastly inadequate, way below capacity spending growth rate for our economy. This is one of the things that worry me about macroeconomists convincing our government to adopt some more-or-less arbitrary target number for spending growth.

DeleteAnd the claim that NGDP growth has been where it is because of "the remarkable job" the Fed is doing is made without any supporting empirical evidence at all - as though there are only two possible causal factors that could contribute to spending growth: fiscal policy and central bank policy.

I have to agree with David. Krugman has been arguing that there hasn't been enough fiscal stimulus. Yet NGDP growth has been at a successful rate of 4-5% each year, which is the implied nominal target of 2% inflation. The economy has hit the macro target. And all this time fiscal policy has been dramatically decreasing. This implies that fiscal policy is irrelevant and that the Fed dominates.

ReplyDelete"This implies that fiscal policy is irrelevant and that the Fed dominates."

DeleteThat doesn't follow. You could just as easily say, "This implies that fiscal policy is so stupendously effective, with a multiplier that lingers over time periods, that it offsets the contractionary impact of later fiscal tightening." Either needs to be backed up with something more.

I suppose that is a possibility. But this would be inconsistent with Krugman's own line of reasoning. He has specifically argued against austerity, arguing it would be bad and would hurt the economy. He does not consider the lingering issue relevant.

DeleteWhat makes something on the order of 4.2% a success

Deletehttp://research.stlouisfed.org/fredgraph.png?g=dtF

when the previous 2 decades, outside of recessions, often ran somewhere north of 6%?

http://research.stlouisfed.org/fredgraph.png?g=dtG

Is this the soft bias of low expectations?

Hi Noah,

ReplyDeleteI think Mr Beckworth has the interpretation of this chart backwards. The chart mixes stocks (gov't exp.) and flows (growth). Clearly, if the stock figure declines, growth rates should be lower but stable, given the standard Keynesian view holds. Indeed, that is exactly what we see: Pre-crisis, NGDP growth was in the 5-7% range, post-crisis and admidst fiscal tightening, it is around 4%. That's evidence in favour, not against, the standard Keynesian view.

cheers

t

t - you are one time derivative too low.

Deletegov't exp is a flow - but the accumulated deficit (perhaps what you mean) is a stock. GDP is a flow. But growth in GDP is a rate of change! But the point is taken, falling stimulus may well take a percentage point off growth!

Is 4-5% NGDP growth considered a "successful" rate in this particular circumstance?

ReplyDeletePlease, David is really arguing that the Sumner critique is the dominant effect. It does not matter what the government does on fiscal, if monetary is active and "targeting" "something" nominal.

ReplyDelete4-5% NGDP consistently sounds like effectively targeting even if they say it as 2% inflation plus as much growth as possible.

Noah's argument is really just trying to turn around the Sumner critique applied to this data to say fiscal could be really effective as in a high multiplier but its offset by opposite and effective monetary since they are sort of targeting. Of course, that's also right. However, fiscal is non-neutral in any way, shape, or form. Government decides who gets the benefits. Why won't Keynesians just admit this is why they like it.

this is seriously schlock economics by Beckworth.

ReplyDeleteFor a more serious treatment, see Valerie Ramey's work.

Also, commentators failed to pick up Noah's key point, that macro aggregates may not be the most useful data.

Microfoundations 5 Schlock aggregate macro 0 (aet)

That's pretty harsh. Is this now going to be considered Schlock Doctrine?

DeleteSchlock and Eeeew.

DeleteOne gets the impression Beckworth may not be familiar with automatic stabilizers which do, in fact, change in real time in response to fluctutations in aggregate demand. As revenues fall stabilizers increase government outlays, and decrease outlays as revenues rise.

ReplyDeleteFirstly there have been no large changes in either fiscal policy or deficits since 2009, with deficits having fallen only from $1.55 trillion to $1.39 trillion in four years. This is due to A) the stabilizers reducing outlays, and B) revenues rising as the private sector recovers.

Secondly it is not useful to judge whether policy is contractionary by looking at the deficit as a percentage of GDP. The economy has been growing for three years, so deficits as a percentage of GDP would fall even if their absolute dollar quantities remained static. Beckworth's graph would lead one to believe we've been engaging in austerity even if the 2011 deficit were identical to the 2009 deficit to the penny, because growth has whittled away at the ratio.

Basic macro: one cannot deterimine budgetary policy by observing budgetary outcomes. It is entitely possible to adopt expansionary policy while experiencing a contraction or vice versa. Beckworth's graphs drastically oversimplify the issue.

automatic stabilizers!

ReplyDeleteNoah,

ReplyDeleteGood rebuttal. My first instinct after reading Beckworth's post was to create similar graphs for that time period displaying monetary policy. As expected, there is very little correlation between the MB or M2 and NGDP over the same time period. Even if the initial logic were correct, it seems the same logic would suggest monetary policy is ineffective. As you put it best, we must be careful of what we infer from these types of graphs.

http://bubblesandbusts.blogspot.com/2012/12/are-fiscal-and-monetary-policy-both.html

Adding to Ben Johannson's comment, with which I completely agree, note that government expenditures have actually been stable after 2009 -- the fall in expenditures/gdp reflects the increase in GDP one to one. Note also that government expenditures seem to have only increased in 2009, accompagnied by increasing growth rates. So if this graph could be interpreted as causal evidence at all (which it actually shouldn't), it is evidence in favor of a large fiscal multiplier, not against.

ReplyDeleteRegarding the identification of fiscal stimulus effects, there is a nice recent literature using IV-strategies and cross-sectional variation to do just that. They usually find quite large fiscal multipliers in the region between 1.5 and 2. See Suarez-Serrato Wingender (http://www.jcsuarez.com/Files/Suarez_Serrato-Wingender-ELFM.pdf)for a particularly nice paper with a very credible identification strategy, and Wilson (http://ideas.repec.org/p/fip/fedfwp/2010-17.html) for estimates of the (job) fiscal multiplier from the ARRA stimulus package.

For those who enjoy sci fi

ReplyDeletehttp://somethingcleverish.blogspot.com/2012/12/starfleet-command.html

Krugman:

ReplyDeletehttp://krugman.blogs.nytimes.com/2012/12/05/evidence-in-macroeconomics/

The "Sumner critique" seems pretty obvious. Say we had a dictatorship instead of executive and legislative branches, the dictator could target an inflation rate via fiscal policy.

Given the example of the epic housing bubble and financial crisis here and in Europe, the data shows that private market and banks did a horrible job of giving out loans, managing risk and allocating resources. So I don't see one should prioritize stimulating demand via the banks and interest rates rather than via the government.

Sam

ReplyDelete"For two years now Krugman has been claiming that we need fiscal stimulus now now now or else EUROPE! Double dip recession!"

No that's mischaracterizing what he and others are saying. They're saying that there's a job crisis with high unemployment and an annual output gap of one trillion dollars according to the CBO. He has argued we need fiscal (and monetary) stimulus to close the gap more quickly and bring unemployment down. Right now things are getting better at a snails pace (or going slightly sideways). It hasn't been worse because of fiscal policy. It hasn't been better because of the anti-fiscal policy of state and local governments.

Krugman and others (like Yellen) have admitted to being surprised at the extent of the "downward rigidity of nominal wages."

http://krugman.blogs.nytimes.com/2012/04/03/screw-your-analysis-to-the-sticky-point/

Automatic stabilizers kick in immediately. How much more rapid can a fiscal policy response be.

ReplyDeleteBeckworth is correct that fiscal policy can be held up by clueless politicians. This is why there are arguments in favor of infrastructure bank and other proposals on revenue sharing with States that would make the response of fiscal policy more rapid. Some fiscal policy UI is rapid. Other is slower than it needs to be. However, that is a problem with the politics, not a problem inherent to using fiscal policy.

-jonny bakho

Surely what this really tells us, in the face of nasty unemployment figures and other things across the time span Beckworth graphs is that NGDP is actually a much less useful statistic than people think.

ReplyDeleteAfter all, let's get this straight - according to Beckworth the years graphed show no evidence of the effects of a great recession at all, despite all the evidence out there in the real economy.

As an aside, the reason NGDP has failed in this instance is because it treats the financialisation of the economy as real growth. Thus QE (in the various forms the Fed is using) works!

DeleteOnly out there in the real economy, it doesn't look so good...

"Automatic stabilizers kick in immediately. How much more rapid can a fiscal policy response be."

ReplyDeleteYes!

Great Post!

ReplyDelete