In my last post, I claimed that the main theoretical framework that people use to think about the Japanese stagnation - the mainstream Woodford New Keynesian model and its baby brother the Econ 102 AD-AS model - didn't apply, because prices couldn't be sticky for 20 years. Paul Krugman agreed that the standard model is inapplicable, but took me to task for forgetting about the liquidity trap.

I didn't forget about the liquidity trap. I just didn't talk about it. Why? Because it's not what most people are using to think about Japan. A liquidity trap may look like something you can just tack on to a standard Woodford or AD-AS model and obtain mostly the same results...but really, it changes the whole thing. And most macroeconomists (that I have seen) are not paying a ton of attention to the Zero Lower Bound; they are still thinking about things in the AD-AS or Woodford paradigm, where unemployment involves things like sticky wages. So that was the paradigm I wanted to address in my earlier post.

I should say that although I haven't ground through the mechanics of a liquidity-trap model, I am favorably disposed toward the models. Why? Because they seem to fit some important stylized facts. The idea of the "paradox of thrift" seems to match what we saw in the U.S. after the 2008 crisis; American savings rates spiked but inflation fell and growth fell, making the resultant deleveraging relatively modest. And the idea that the Zero Lower Bound is real and important seems borne out by the difficulty that central banks have had in creating growth or inflation via Quantitative Easing. Certainly, liquidity trap models are consistent with one important piece of the Japan story: the coupling of persistent deflation with zero nominal interest rates.

{kind=link}

{kind=link}

As I said in the update to my last post, liquidity trap models might be able to explain Japan's stagnation where mainstream New Keynesian/AS-AS models fail. Liquidity trap models might have multiple equilibria, or very very long-lasting impulse responses to demand shocks. I'm not sure whether they do have these features, but it seems that they might. And they might contain some reason why Japan might be more susceptible to a super-long deflation than other countries.

BUT, here is the thing about liquidity trap models: They are not yet well-developed or well-explored, compared to other kinds of models. The liquidity trap is the subject of only a few theoretical papers that I know of. The main fully-specified NK-with-liquidity-trap DSGE model I know of - Eggertsson & Woodford 2003 - doesn't even include capital investment or supply shocks. And very few researchers have yet tried to take the model to the data to see how well it fits in general (as opposed to simply "explaining" the stylized facts it was invented to explain). This is in contrast to the Woodford/AD-AS paradigm, which has been very thoroughly explored by many many macroeconomists for decades. We know all about how Woodford/AD-AS works. But there are many things about liquidity trap models that we don't yet know or understand. And these gaps lead to puzzles when we try to apply the theory to the real world, even in a casual manner.

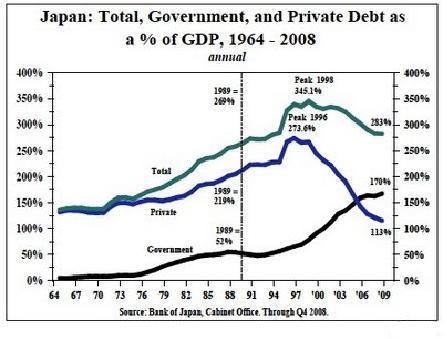

For example, the strong form of the Paradox of Thrift says that the private sector's attempts to save more will mostly be thwarted. But Japan has successfully deleveraged since its 20-year deflation began! Check it out:

That is a huge, steep, sustained fall in private-sector debt (the blue line) starting in about 1999 (note that it's a debt/GDP ratio, so this is in real terms). By the eve of the 2008 crisis, Japan's private debt was lower than at any time since 1964. And all through that successful rapid deleveraging, there was indeed deflation. And after that massive deleveraging, deflation or ~0% inflation continued.

That's not a result you would expect from knowing the Paradox of Thrift. It may well be that this sort of thing can happen in a liquidity trap model - it may not be a true "puzzle" or "anomaly" - but you wouldn't guess this from the basic intuition.

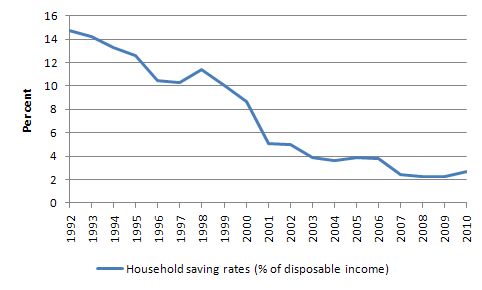

Another Japan puzzle for liquidity trap models is that Japanese households don't seem to behave the way that the models expect them to. During Japan's long deflation, household saving rates fell dramatically:

This is NOT what households are supposed to do in a liquidity trap, right? Japan's increase in private saving has all come from corporations. And I suppose you could wave a hand and say that the "representative household" owns the "representative firm" and makes corporate savings decisions. But even with increased corporate saving, Japanese savings rates fell during the deflation:

To my knowledge, liquidity trap models don't (yet) model the saving behavior of firms, since they don't (yet) include capital investment. They also don't (yet) model the effects of supply shocks in a liquidity trap; this is probably relevant for Japan, since its economy experienced a boom in 2002-2006, probably driven by increased trade with China, during which time interest rates and inflation both stayed around zero. Therefore, though falling private savings rates might not fit with the basic Eggertsson & Woodford (2003) liquidity trap model, it is not yet known if this would present a puzzle for an expanded, generalized model.

To my knowledge, liquidity trap models don't (yet) model the saving behavior of firms, since they don't (yet) include capital investment. They also don't (yet) model the effects of supply shocks in a liquidity trap; this is probably relevant for Japan, since its economy experienced a boom in 2002-2006, probably driven by increased trade with China, during which time interest rates and inflation both stayed around zero. Therefore, though falling private savings rates might not fit with the basic Eggertsson & Woodford (2003) liquidity trap model, it is not yet known if this would present a puzzle for an expanded, generalized model.

But that aside, here is really my fundamental issue. In a standard Woodford New Keynesian model, we know how long recessions can be expected to last without policy intervention: less than 5 years. In the liquidity-trap models, the characteristic length of a recession without policy intervention is not clear. Do recessions always go away on their own in a liquidity trap model, or does the economy get stuck indefinitely in a "bad equilibrium"? And recessions do go away on their own, how long does that usually take? I think this question needs answering before liquidity-trap models become our mainstream, go-to intuition about how the macroeconomy works.

Eggertsson & Woodford (2003) include some impulse response graphs, and it definitely looks like the effect of a shock decays in less than 5 years, just like in a standard Woodford New Keynesian model. However, those impulse responses are conditional on a policy regime that may not match what we see in real life. So the answer to the question of "How persistent are demand shocks in a liquidity trap model?" remains unanswered.

If it turns out that DSGE liquidity trap models don't produce stable "bad equilibria" or very very persistent impulse responses to demand shocks, then explaining Japan's 20-year-stagnation with one of these models will require the assumption of a whole string of negative shocks...just like their mainstream New Keynesian and RBC cousins.

Eggertsson & Woodford (2003) include some impulse response graphs, and it definitely looks like the effect of a shock decays in less than 5 years, just like in a standard Woodford New Keynesian model. However, those impulse responses are conditional on a policy regime that may not match what we see in real life. So the answer to the question of "How persistent are demand shocks in a liquidity trap model?" remains unanswered.

If it turns out that DSGE liquidity trap models don't produce stable "bad equilibria" or very very persistent impulse responses to demand shocks, then explaining Japan's 20-year-stagnation with one of these models will require the assumption of a whole string of negative shocks...just like their mainstream New Keynesian and RBC cousins.

So to sum up: No, I did not forget about the liquidity trap. And I kind of like the liquidity trap idea. I think liquidity traps are a candidate explanation for how demand shocks might have extremely long-lasting effects. But I do not know enough about the models to say that Japan's unusual situation can be explained by demand shocks + a liquidity trap. If the models require a long string of exogenous, hard-to-observe negative demand shocks in order to produce what we've seen in Japan, then I'm going to be very very skeptical. If, on the other hand, the models give some reason why some special Japanese characteristics - Shrinking population? Stagnant productivity? High levels of "patience"? - make a 20-year response to a single big demand shock a conceivable reality, then count me as a (tentative) believer.

Update: Steve Williamson and Matthew Martin both chime in with good posts that play around with the implications of liquidity-trap New Keynesian models. Both posts show how little of the standard New Keynesian intuition applies with liquidity traps, and how little we understand about the true general behavior of these models.

Update 2: Someone also reminded me of this paper by Mertens & Ravn, who find that liquidity trap models can sometimes cause supply and demand factors to become entangled, just as people like Tyler Cowen, Scott Sumner, and I have intuitively suspected in the case of Japan. The paper also shows, yet again, how many things we are still learning about the general behavior of the models, and their sensitivity to different assumptions and situations.

Update: Steve Williamson and Matthew Martin both chime in with good posts that play around with the implications of liquidity-trap New Keynesian models. Both posts show how little of the standard New Keynesian intuition applies with liquidity traps, and how little we understand about the true general behavior of these models.

Update 2: Someone also reminded me of this paper by Mertens & Ravn, who find that liquidity trap models can sometimes cause supply and demand factors to become entangled, just as people like Tyler Cowen, Scott Sumner, and I have intuitively suspected in the case of Japan. The paper also shows, yet again, how many things we are still learning about the general behavior of the models, and their sensitivity to different assumptions and situations.

Noah,

ReplyDelete"The idea of the "paradox of thrift" seems to match what we saw in the U.S. after the 2008 crisis"

The paradox of thrift is what occurs in any NK model if the real rate is not lowered to the level of the natural rate. The ZLB just forces that to happen.

"liquidity trap models mightbe able to explain Japan's stagnation where mainstream New Keynesian/AS-AS models fail."

Huh??? You know that the standard liquidity trap model is just the standard NK model with a particular nominal rate rule, right? (One where nominal rates must be positive.) What "mainstream NK" model do you have mind? One where contrary to reality, rates in Japan weren't stuck above zero?

"Liquidity trap models might have multiple equilibria, or very very long-lasting impulse responses to demand shocks. I'm not sure whether they do have these features, but it seems that they might."

I don't even know how to begin to parse this...the liquidity trap is just a nominal rate rule. It's not some kind of special model. You can implement the standard NK model with any number of rate rules. If you understand the NK model, the liquidity trap is not some mysterious thing with possible "multiple equilibria, or very very long-lasting impulse responses to demand shocks." Its *just* a particular set of exclusively positive rate rules for whatever is your favorite NK model. You can even study liquidity traps in perfectly competitive rbc models. See eg posts by Cochrane or Andolfatto. The liquidity trap is a necessary fact of any model where the CB sets the nominal rate and inflation does not increase in response to surprise hikes of the short rate (and nominal rates can't be negative). It really is that ubiquitous and not exotic at all.

"The two seminal papers"

Uh, no. Krugman 98, was actually seminal. But Eggertsson and Krugman was definitely not. It was yet another liquidity trap model with special features. And there are plenty of liquidity trap models with capital that existed well before 2011.

"This is in contrast to the Woodford/AD-AS paradigm, which has been very thoroughly explored by many many macroeconomists for decades."

OK, what is "Woodford/AD-AS"? How can this model be so well understood, yet so much mystery surround what happens if rates can't go negative? Woodford, to me, just means NK.

"In a standard Woodford New Keynesian model, we know how long recessions can be expected to last without policy intervention: maybe about 5 years. In the liquidity-trap models, the characteristic length of a recession without policy intervention is not clear."

What does "without policy intervention" mean? If you mean without lowering rates, then that's a liquidity trap. I you mean with lowering rates, then why would you have a recession?

Other things too, but enough for now. I really can't make heads or tails of this post.

This idea that liquidity traps are "just" NK models with different nominal rate rules is a bad idea. The nominal rate rule is extremely crucial in any NK model, as you well know. Changing that rule changes all kinds of other properties of the model. To claim that this is a small difference that can easily be intuitively understood is just hand-waving.

DeleteBut it's not a rule change: it's just what happens when one particular value gets entered which is not, in reality, possible. Just follow the implications of that in the standard models and presto! Liquidity trap.

DeleteNot a big fan of models or Keynesian theory here, but before you go looking, be aware that Krugman in his early writings about Japan invented his own definition of liquidity trap, in which the zero nominal bound and low inflation prevent real interest rates from adjusting low enough to spur sufficient investment. These days most people follow Krugman's definition, but if you're digging for academic models, you may bump into the early Keynesian definition, based on an aside in Keynes' general theory, where he warns that if long rates were very low then liquidity preference could dominate over reward for risk.

ReplyDeleteThe strong version of the paradox of thrift applies when everyone saves at the same time. Clearly from your graph, the govt was DIS-saving at the same time that the private sector was saving, thereby enabling the private sector deleveraging.

ReplyDeleteAs your chart also shows, overall debt (incl public sector) has also fallen (far more gradually) as a share of GDP since the late 90s, even as nominal GDP has stagnated. Partly this is due to Japan's current account surpluses, which have shifted the burden of excess Japanese savings onto the rest of the world. It may also be in part due to the household sector running down their capital (e.g. retirees spending their pension pots), enabling the corporate sector to deleverage.

The behaviour of the household sector is also no puzzle. After the bubble burst, it was the corporate sector that was left with a load of unrepayable debts. The household sector were big net savers, with very little debt on their balance sheet. High real rates have therefore increased household wealth, and this wealth effect explains the slow increase in real spending (and indebtedness) of the household sector. The dissaving of the corporate sector is exactly what you would expect - after the bubble burst, their priority became solvency and debt repayment, rather than profit maximisation and investment.

Noah,

ReplyDelete"This idea that liquidity traps are "just" NK models with different nominal rate rules is a bad idea."

Well, it is both correct, and perfectly relevant to the points I was making. All of which you ignored.

Again:

"liquidity trap models might be able to explain Japan's stagnation where mainstream New Keynesian/AS-AS models fail"

The difference between what you call "liquidity trap models" and what you call "mainstream NK/AD-AS" models is, apparently, ZLB vs Taylor rule. If your point is that Taylor rule models aren't very good at explaining Japan... well no shit! Newsflash: Japan hit the ZLB, and QE doesn't doesn't produce inflation *contingent on the path of the short rate* (i.e. at the ZLB). That is a feature of basically *any* arbitrage free model you can write down, and, at this point, an empirical fact. If you are going to use NK as your model for an economy YOU HAVE TO USE THE SHORT RATE IN THAT ECONOMY. So you can't *choose* between "liquidity trap models" and "mainstream NK/AD-AS". It's the same model!

"In a standard Woodford New Keynesian model, we know how long recessions can be expected to last without policy intervention: maybe about 5 years."

What does this mean? As I said, in the standard model we don't have recessions because there is no trade off between controlling inflation and the output gap, and no constraint on the short rate. There are any number of tweaks that produce optimal policies with recessions. But those are not "standard."

Look, you stepped out of your comfort zone, said some stuff that wasn't very coherent, and ticked off Paul Krugman. You should probably have taken a step back, but instead you dug in, and now, I'd say, you getting yourself further into deep water. The truth is, of course, that there are very real limits to what the NK model can capture in a deep liquidity trap (and maybe I'll write a comment touching on that below), but you are not making any progress towards addressing that in this or the previous post.

Well, it is both correct, and perfectly relevant to the points I was making. All of which you ignored.

DeleteWell, to be brutally honest, I thought most of your earlier comment wasn't that coherent...

The difference between what you call "liquidity trap models" and what you call "mainstream NK/AD-AS" models is, apparently, ZLB vs Taylor rule.

Well, some people think that if the central bank is very good at managing expectations, it can approximate the effect of a Taylor rule even with the ZLB there, and thus set real rates to be whatever it wants. This is what a lot of monetarist blogger types seem to have in mind.

What does this mean?

Just look at the impulse responses to a policy shock in at Woodford model, dude.

ticked off Paul Krugman

He's not ticked off.

You should probably have taken a step back, but instead you dug in, and now, I'd say, you getting yourself further into deep water.

All these metaphors are telling me that you see econ blogging as sort of an intellectual pissing contest. And yeah it's fun sometimes to argue and troll, but sometimes you just want to have a conversation with people and figure out what's going on. I guess you can't understand that...

Wait, so "K" isn't Krugman? I am newer here, so I may have missed something...?

DeleteMore importantly, I see an informed description of what Noah Smith is describing in his posts on this point, but I fail to see HIS actual opinion on what it means or what we should do about it...?

Lastly, does the wealth gap widening in Japan during the last many years explain the liquidity-trap/sticky-prices/private-sector-savings-rate-decline phenomena? Is this not what we are seeing (will be seeing more of) in America?

Yeah, Noah, I'm pretty sure K is Paul Krugman

DeleteWhy do you think "K" is Krugman? What I read is someone trying to emulate his style and not doing a very good job at it.

DeleteThis comment has been removed by the author.

DeleteJam,

DeleteOne does not edit their response to blogs like they edit their posts as author's.

Who do you propose K is? Their knowledge and ability to draw creative and relevant assumptions on Noah's work is extremely high-level and coherent. If it's not Krugman, I want to know who it is so I can read more from them.

When I read this post, I felt kinda dumb because I didn't understand any of it.

ReplyDeleteThen I read that Krugman doesn't get it either, so...

Yeah, I had the same response. Read it twice trying to absorb the arguments, then gave up when I realized it actually doesn't really make coherent sense.

DeleteWhat's hard to understand?

DeleteNoah just said that in a standard NK model you don't get enough persistence to explain a 20-year stagnation from a demand shock. Krugman said, approximately, "Ah, but you forgot about the liquidity trap!" Noah responded by admitting his ignorance (an admirable quality!) of the technical details of a ZLB in a NK model, but professed his belief that this did not alter his fundamental point.

And I believe that Noah is correct: In modern NK models with a ZLB, with the parameters people actually use, you don't get 20 years of persistence from a demand shock.

It seems Krugman has a different model in mind, which may in fact be closer to what Keynes had in mind in the GT, but isn't quite the same as the main models people use nowadays to describe these phenomena.

Ramsey, Your understanding of the interaction between Noah and PK is good. And I agree with you that Noah is on to something here. Especially when he brings up how savings rates fell during Japan's liquidity trap. One would assume that savings rates would rise.

DeleteNoah wants a deeper discourse. My view is that this is all heading to a deeper understanding of how declining labor income causes the stagnation. PK is mentioning how across-the-board wage reductions don't help. That comes from Keynes. And we see labor share falling consistently in Japan from 1990.

My view is that Noah is pushing a thought about Japanese stagnation that could lead to PK having an illumination on the subject. PK is close to understanding the effect of declining labor share (as opposed to capital share), but from his writings and videos, PK just hasn't wrapped his head around it yet. He made reference last month in a debate on inequality that we need more research on the inequality between labor and capital income.

Hopefully Noah has nudged him closer to a better understanding.

Ramsey, "And I believe that Noah is correct: In modern NK models with a ZLB, with the parameters people actually use, you don't get 20 years of persistence from a demand shock."

DeleteYou have the fatal caveat right there. Perhaps the framework of the NK models is correct, but people need to look at a larger parameter space to get to the persistence.

This comment has been removed by the author.

ReplyDeleteModels don't just fail because they make incorrect predictions but also because the modes of thought they encourage are a "dead end" (i.e., Ptolemaic epicycles vs. heliocentric model).

ReplyDeleteThese fancy-schmancy DSGE models just lead to confusion. I have a pretty good intuitive idea of what's happening in Japan. There is a hypothetical bad equilibrium -- essentially a speculative bubble with money as the bubble asset, although, since money is the unit of account, most people think of the bubble as a "loss of confidence" in everything except money -- but you never really get to the bad equilibrium (we kind of did in 1929-1933, until devaluation popped the bubble), because central banks (which either won't or can't do what's needed to pop the bubble) stir up the water as much as possible to avoid moving toward equilibrium, and also because nominal wages are sticky downward, which slows down the progress of the bubble, and also probably because, if the bubble were allowed to progress, people would eventually realize that it's silly to hoard an asset without intrinsic value. (The 1929-1933 contraction was essentially a bubble in monetary gold. I imagine that bubble would eventually have ended on its own, as people realized how ridiculous the value of gold was getting relative to everything else, but it might have taken a whole lot of deflation to get to that point.) The ability to capture my intuition in an DSGE model is limited, because we're always far away from the actual bad equilibrium. Maybe a DSGD model, but that's even more confusing.

ReplyDeleteWhat happens to risk of return on investment when demand collapses and utilization is far below capacity?

ReplyDeleteRisk skyrockets. Risk is not static and risk that has skyrocketed due to slack demand cannot be reduced enough by monetary easing to encourage enough investment. It becomes obvious that risk must be reduced and that increasing demand is required to reduce the risk. However, demand will not increase until people have jobs. The incentives are perverse.

Demand after a severe recession can take a long time to return. The key, then is to increase short term demand enough that it lowers risk; lower risk increases investment and the higher velocity of money becomes sustainable.

Resources must be reallocated to increase demand, either by BigG outright purchases of goods and services or increase in labor demand by BigG to deliver additional public goods and services. Unfortunately, we have a situation in much of the world where popular opinion is against public goods and services, a stance that leaves everyone worse off. Japan has simply not shifted to producing a combination of goods and services for export or internal consumption that match their labor capacity. There are plenty of goods and services that would improve life in Japan. Some agent (BigG is the likely candidate) must serve as agent for increase in demand.

jonny bakho

Very astute.

DeleteWe are in a situation where the Fed has responded to the collapse of demand in a way designed to combat very low demand. The only problem is when you enter a zerobound economy, the Fed through monetary policy can only control remotely the level of the asset pricing, and has almost no control over actual growth of the economy.

Now, we see monetary policy generates almost no inflation, as assets bought for cash pushed into the financial system artificially keep asset prices high, but provide no incentive and no stimulus to the labor portion of the economy.

In short, business was saved in 2008, but now sees low demand, and so chooses small levels of investment in response to a much lower level of demand.

Without the pressure and ruination of a stock market crash and constant bank failures, the political system refuses to provide any significant stimulus to the system through massive labor programs, and without it, we live in Japan.

In short, we are still facing the same situation as in the previous post, an economy that appears healthy, but is in reality much smaller than it used to be, and the political solution is unreachable.

So, while we might waste a large amount of money on road construction, most of it will not generate significant employment and wages, which are necessary to generate retail demand for, well, everything. With 47 million on foodstamps, we can essentially say a significant portion of our population is simply not involved in the economy beyond mere survival.

That alone should be very disturbing to people, because another shock to the system would at this time, quite possibly be more than the system could take and remain intact.

In short, the best run solution at this is Japan, the worst is Argentina, and yet we dither about making strategic long run solutions or hope for a huge alien invasion to finally force employment on the unemployed through desperate demand.

As long as capital strangles the political system in the goal of wealth preservation, we will see capital driven to increasingly risky strategies to generate return, with periods of capital destruction.

In short, not only are we at the zerobound, we face a Japanese style demographic headwind that dictates the baby boomers increase savings, and then spend that same savings, without significant savings coming from younger generations.

Zombie level economics.

If one wants to read the right papers now from the depression, one can reread Fisher, and see how right he was once he recognized his earlier failures.

Nice, I have never really thought about "risk" quite this way before. I will now.

Delete+1 to Bill Ellis. I agree with the phenomenon (low demand makes business investment pointless ; see:

Deletehttp://theredbanker.blogspot.com/2013/03/refreshing-macro-part-4-profit-matters.html

but I had not thought to call it 'risk'. It's an interesting idea - even better, imho, call it 'business risk' as in "in a low demand environment, business risks skyrocket and low interest rates don't change that"...

Well said, Citizen AllenM.

DeleteI am confused... (what's new? ) My little non-economist brain sees some things in this post as contradictory. Are they ?

ReplyDeleteA)..."For example, the strong form of the Paradox of Thrift says that the private sector's attempts to save more will mostly be thwarted. But Japan has successfully deleveraged ( decreased public debt as a share of GDP )since its 20-year deflation began! Check it out:"

then...

B)..."Another Japan puzzle for liquidity trap models is that Japanese households don't seem to behave the way that the models expect them to. During Japan's long deflation, household saving rates fell dramatically:"

And...

C)... "Japan's increase in private saving has all come from corporations."

OK...So isn't B consistent with A ? And isn't declining debt NOT the same as saving in this case ?

Also... Keynesian Ideas about the liquidity trap should not be expected to function well when the economy has been distorted by institutionalized elite rent seeking...right ? Perhaps what shows up as inconsistencies with Liquidity trap models are the result oligarch excess ?

I am surprised none of the M&M's (Market Monetarists) have shown up yet to tell us that none of this liquidity trap "mumbo jumbo" means anything.

ReplyDeleteWe're seeing the same thing in the USA: slow growth, multinationals hoarding money and consumers reducing savings. I guess there could be a lot of hidden inflation eating away at the savings of households that economists don't see. I would surmise that neither the USA or Japan has a true liquidity trap.

ReplyDeleteLack of income can lead to a lack of savings. You cannot save what you do not earn, and unemployment and underemployment are affecting a significant number of otherwise potential consumers/savers. As for large corporations, they are seeing high profits with little incentive to expand -- hence they "save". No need for "hidden inflation".

DeleteWhat Anonymous said. But I would add 'hidden inflation' anyhow. Oil and food prices, volatile though they may be, matter.

DeleteJapan has, for all this time, had an active, independent monetary policy with a floating exchange rate. It's not locked into some other country's monetary policy. Hence "0% forever" has to be viewed as an eccentric policy choice, not something external. The BOJ is (or at least was until recently) acting like stabilizing interest rates (not prices, or the economy) is its top priority. What effect does this have? Who knows?

ReplyDeleteGood point. That "0% forever" is ultimately a policy choice is often overlooked by economists.

DeleteNoah - what about Richard Koo's idea of a "balance sheet recession"? Do you think that might offer a workable explanation of Japan's lost decade? It has some similarities to the liquidity trap idea, but differs by placing more emphasis on debt and deleveraging.

ReplyDeleteParadox of thrift would not fully apply to a country integrated into world capital markets with a floating exchange rate.

ReplyDeleteRapid private sector deleveraging is not a counter-example if at the same time the government is borrowing huge amounts and running deficits. The total net deleveraging appears to be about 4% of GDP per year for 15 years. Part of that will be write-offs of bad loans rather than actual savings.

The long persistence makes perfect sense in the context of the old school IS/LM model (I know...). You got a vertical AD curve, moved back by a bad IS shock. SRAS can shift around all it wants to, prices getting un-sticky and all. Doesn't matter. The LM curve just stretches. That's the "trap" part of the "liquidity trap".

ReplyDelete(of course that has some problems of its own, like the entire LM curve but I suspect this is what motivates Paul's intuition on Japan)

(Edit: before hitting "Publish" I thought it wise to google "liquidity trap vertical AD curve" really quick and found this old conversation: http://macromarketmusings.blogspot.com/2008/12/paul-krugman-and-vertical-aggregate.html . So yes, I think this has been at least partly covered before)

At least in the Eggertson/Krugman liquidity trap model, the AD curve is not vertical - it's actually upward sloping (ie., backwards).

DeleteNoah, in your "Japan's stagnation: demand-side or supply-side?" post you ask ..."Is it possible for a negative shock to push a country into a bad liquidity-trap equilibrium, out of which it cannot escape unless it receives a big "kick" (from policy or from a positive exogenous shock)?"

ReplyDeleteKeynes thought so...( I am sure you have seen this ).

From the last paragraph of "THE GREAT SLUMP OF 1930" By JOHN MAYNARD KEYNES...

"...agriculturists and householders throughout the world, who have borrowed on mortgage, would find themselves the victims of their creditors. In such a situation it must be doubtful whether the necessary adjustments could be made in time to prevent a series of bankruptcies, defaults, and repudiations which would shake the capitalist order to its foundations. Here would be a fertile soil for agitation, seditions, and revolution. It is so already in many quarters of the world. Yet, all the time, the resources of nature and men's devices would be just as fertile and productive as they were. The machine would merely have been jammed as the result of a muddle. But because we have MAGNETO trouble, we need not assume that we shall soon be back in a rumbling waggon and that motoring is over."

http://www.gutenberg.ca/ebooks/keynes-slump/keynes-slump-00-h.html

Magneto problems. I remember back when this depression first started, Krugman kept trying to get this concept across. I think the outdated metaphor makes it a hard job. I think maybe "starting a lawn mower" might have been better. I dunno.

Oooo... I like this metaphor for "the magneto problem"... State change.

DeleteLike this... If the economy is frozen like ice, It does not matter if we go from zeroº to 31º.... it is still too cold. We must set the thermostat to at least 33º to get things flowing.

And it fits nicely with other commonly used econ metaphors... Like, "the economy is over heated. so beware inflation "

A proponent of stimulus could say, "The economy is frozen, we need more fuel for the fire". Inadequate stim could be explained like this... "This stim too small. It will make the economy warmer, but it will not make it hot enough to melt the ice."

See, by using the already common temperature metaphor, I think it makes more sense on gut level. ( Or, if you disagree with the concept of magneto trouble, it makes it easier to believe a lie...I guess .)

I think a better analogy is "critical mass." Actually, it's barely even an analogy - "critical mass" systems (ie systems that experience "network effects") include everything from internet start-ups, to nuclear bombs, to macroeconomic stagnation.

DeleteBecause this description correctly conveys the way these systems behave - water is a non-flowing solid whether it is 10% of the way to state-change (32) or 90% of the way. But in a critical-mass/network-effects system, you do see a significant difference between 10%-to-critical-mass vs 90%-to-critical-mass. But until you get to 100%, the "reaction" (whatever it is) is "unsustainable."

Why?

That's where the "network-effects" come in. "Critical-mass" is just a way of describing how many parts/people/atoms are in the vicinity of any other parts/people/atoms - and the more their are, the greater the probability that any one of these "nearby" things will interact - whether that's exchange money, exchange neutrons, or exchange information.

When too-little fuel is getting ignited to start an engine, the engine may still turn over - it just won't start up a self-sustaining cycle. Similarly, if stimulus is too small it doesn't completely fail - it still causes an increase in incomes and available jobs, etc, temporarily - but it fails to trigger enough long-term hirings to keep the economy growing once it is withdrawn.

"Another Japan puzzle for liquidity trap models is that Japanese households don't seem to behave the way that the models expect them to. During Japan's long deflation, household saving rates fell dramatically: This is NOT what households are supposed to do in a liquidity trap, right? Japan's increase in private saving has all come from corporations."

ReplyDeleteLooking at the current situation it seems that on average most "consumer" households have less disposable income (due to increased unemployment or under employment -- hence less ability to save) while corporations and high-end private investors have more profit and less incentive to expand or invest, hence more incentive to save. The only ones *with* the ability to save more are the corporations and high-income private investors. Does that mesh with Japan? How might you model that?

A couple of points, long and short term.

ReplyDeleteLong term, it doesn't strike me either of the models here are terribly well explained, or their Japan connections clarified. My own work has been called "incoherent" enough times for me to know that my some ideas are too portentious to be worked through easily, however many endorphins per session. There are likely, almost certainly, many papers examining Japan from either perspective you take; not that they've emerged in macro classrooms, or have been read by sufficient interlocutors. The hundreds of economics journals SUNY doesn't subscribe to are a huge resource for valid science; and I hope you'll get a chance to trek down to NYU or Columbia for some speed reading practice, or "systematic review," as it's called. Long term.

Short term though, you have a shocking problem!

Persistence really isn't an issue if the shocks keep on coming. Mesoeconomic shocks, industry by industry, to Japan's monopolistic positions would seem more characteristic.

Sigh...

ReplyDeleteThere is an elephant in the Japanese room so far unmentioned in either this post, the one before it, in the reply by Krugman, or in any of the comments, although Andrew Harkness almost got it. That is the residual hangover of the collapse of the Japanese real estate bubble in helping to maintain the liquidity trap state. On the original question raised in the last point, I think those raising the demographic issue have it, with the declining population in fact operating both on supply and demand.

So, when the Japanese real estate bubble finally peaked about a year and a half after the stock market bubble did, in mid-1991, it began a long slow decline. In correspondence with Charles Kindleberger at the time, he noted to me that this was the first bubble he was aware of in all world history that was going down more slowly than it went up, and I think he was correct. Nobody has provided a proper explanation of this, although I once refereed a paper that failed to get published that claimed that the Japanese banks were manipulating the real estate decline to slow it, given the enormous amount of real estate on their books, with an eye to prop themselves and the entire Japanese keiretsu system up, which involves de facto conglomerates centered on the banks.

As it is, the real estate bubble was enormous, with it easy to foget the wild stories from the peak of how the imperial palace grounds in central Tokyo were worth more than the entire state of California or how as real estate metro Tokyo was (nominally on paper) worth more than Britain, France, and Germany combined. Of course, that was always nonsense given that if there had been a real effort to seriously cash in on any of that, the prices would have collapsed and the illusion of all that "fictitious capital," to use a classical economics term for a bubble, would have been revealed. In any case, for whatever reason, after it "popped" (that term you like so much, Noah), this enormous bubble behaved unlike any other in world history anywhere, and the decline is still going on.

Now, there was a moment when it appeared the gradual real estate price decline had ended, around 2005 or so. I spent a month there then, and in central Tokyo real estate prices were actually rising. However, that was also the point of maximum Japanese population. The appearance of actual population decline appears to have restarted the decline of real estate prices in central Tokyo shortly thereafter, with the decline never having halted in most of the nation. In any case, it is not at all hard to see how this ongoing backdrop phenomenon feeds into aggravating the tendency to a liquidity trap.

BTW, the obvious solution would be for the Japanese to be more open to immigration, but even Brazilian-Japanese immigrants, who have been specifically favored due to their ethnicity (Brazil has by far the largest ethnically Japanese population in the world outsiide of Japan), have been returning home due to percevied economic and social discrimination. Maybe Abenomics will kick them into a better basin of attraction, but there are some powerful forces holding them in the unfortunate one they are in now.

It seems to me that as the bubble inflated it would inflate GDP numbers with the result that when we compare pre and post bubble reported growth we may be using an entirely false pre-collapse baseline.

DeleteSo if connect real estate bubble and demographics, real estate bubble was driven by asset accumulation during peak earning years, then the a) deleveraging and b) decline in spending aren't that hard to explain. As Japanese got older, they a) paid off the mortgage and b) started to spend down savings.

Deleteread "decline in saving"

DeleteThe key to understanding Japan's Lost Generation is that fictious private wealth from real estate has morphed into fictious private wealth from government.

DeleteJapanese knew and didn't know that their late 80s real estate wealth wasn't real. They knew that very little of it could be sold for yen, yet they treated their paper wealth as real, and spent and speculated accordingly.

Fast forward a generation. Nowadays ordinary Japanese know that the government's $10 trillion of public debt will not be paid back in real terms. Hence they know that the holders of this debt do not really hold the paper wealth that they claim on their balance sheets. Yet, Japanese continue to go about their daily lives with the fiction that this public debt, is, in fact, real, and that it will be repaid. And this, more than anything else, is what has killed the animal spirits of the private sector.

Abenomics shakes this matter up a bit, but not enough to really move the needle.

Japan must be understood as a nation that lived through the greatest asset bubble of the century, and as nation that papered over the bursting of this bubble with endless public debt.

Because Japan borrows in its own currency, this game will not end until Japanese people say it must. Until Japanese insist that the fake wealth ends, and allows real values to clear, the nation's Hansen-like secular stagnation will continue.

Any NK model that fails to incorporate the covering up of the post-Bubble Economy will lead to wrong-headed conclusions.

Nick R.

Kyoto

"But Japan has successfully deleveraged since its 20-year deflation began! Check it out:"

ReplyDeleteI think this maybe creating your issue. Japan's general government debt as a % of GDP jumped from 67% in 1991 to 230% in 2011. Japan's consumer debt to income ratio which provides a more useful insight into the way in which consumers interact with the economy has not changed much in the last 20 years. In 1990 it was 118% and in 2011 117%. It peaked at around 126% in 2001. In essence there has been very little deleveraging of Japanese consumers. See link to OECD data

http://www.oecd-ilibrary.org/sites/factbook-2013-en/03/03/02/index.html?contentType=&itemId=/content/chapter/factbook-2013-28-en&containerItemId=/content/serial/18147364&accessItemIds=&mimeType=text/html

Tom, You add an important thought here. In Noah's graph, private debt to GDP fell. Are you saying that was all firms? That firms have deleveraged but consumers have not?

DeleteConsumers must have constrained liquidity to not be able to deleverage and then have household savings rates fall.

Yes, that's a reasonably accurate picture. There's a round 3X corporate liabilities outstanding vs consumers' hence the fall. Japanese firms have deleveraged almost a third since 2006 which was roughly the level reached at the peak of the bubble in 1989. Although consumers have deleveraged a little since 2006, they are still at similar levels they were in 1990.

DeletePerhaps firms can afford to deleverage more than consumers? More money flowing into profits, and not enough into wages? Also, what is Japanese bankruptcy law like? Is it easier for firms to walk away from debt than individuals (or less loss of face)? Would bankruptcy result in "debt elimination" in a way that would look like deleveraging?

DeleteDefault rates in Japan have always been much lower than in the US. This is why the CDS market trades at roughly a third of the level the US trades at. Although when JAL defaulted it did cause the market to shift up slightly. Japanese companies are on average 50% less profitable than US firms in the way they deploy capital ie profits are not particularly robust, but there maybe something to your point on income to labour being lower than income to capital. This seems to be a global phenomena.

DeleteNoah, when you said, "That is a huge, steep, sustained fall in private-sector debt...," notice that the decline you cite was almost a 1-for-1 *transfer* of private debt to government debt. The slopes are roughly equal - and the %-of-gdp changes were fairly similar (~125%... just eye-balling it). Yes, "total debt" fell. How/Why? A favorable trade imbalance, of course.

ReplyDeleteBesides, "The Paradox of Thrift" does not mean that thrift gets you literally nothing for your effort. If I, as an individual, retain my job but cut my spending and work to pay down my debt - I will be successful so long as I retain a job at (or above) whatever my income was when I started saving - so my personal debt will decline.

However, my reduced spending means a reduction in circulating capital throughout the rest of the economy - and that means (somewhere) someone is earning less (or nothing) as a result - *unless* my creditors use the money I use to pay them to loan out to someone else. But if an economy is already stagnated and almost everyone with an income is paying off debt rather than taking more on, creditors can't find people to loan money to even if they want to - even if they provide loans at rock-bottom interest rates. Because if "George" is cutting expenses and reducing his debt - he's doing it for a reason. What would be the reason? Of course, the reason tends to be that maintaining the debt is suddenly over-extending George - or George is worried he'll be laid-off and then really will be over-extended.

Also, The Paradox of Thrift absolutely can lead to exported debts via a trade imbalance. And this is not a cop-out of an "open-system." The system (or flow) is, actually, closed - and the "paradox" is fulfilled just as soon as the nation(s) doing the importing realize that their trade deficit vis-a-vis Japan (in this case) is leaving *them* with too much debt - so they cut back *their* purchases - and that ripples back to slowing down the Japanese economy. This is ultimately how and why The Great Depression was a global event, not just a national or western-nations-only event. For some nations and regions, the capital-circulation slow-down has a longer lag-time. But the result and cause is always the same, though it is, perhaps, more clear to restate the thrift paradox as:

"By 'thrift' we mean 'aggregate thrift' - and by *that* we mean the difference between the purchase of goods and services vs the change in debt - and to the degree any "system" - national, global, municipal, hydrodynamic flow, rat breeding flow - *whatever* - experiences a net reduction in purchases(/outflow) relative to debt(/pressure) - there must be a corresponding change in income(/inflow)."

Put this way, you can see that we aren't talking about a theoretical concept. This is simply the nature of all "flows" and it applies to everything that can be called a flow (ie, when it comes to atoms: everything that is subject to the Pauli Exclusion principle...).

You are describing the effects of over leveraging. The cure for over leveraging is inflation. People have too much debt to income. Prices (in this case housing bubble) have deflated leaving debt subject to default. Inflation, especially wage inflation, allows the bubble prices to relatively reset with less default and reduces the outstanding debt to income ratio. Inflation has the least bad consequences to labor. It is only the malefactors of great wealth who wish to protect the value of their loan portfolio (gained in part by making bad loans) who fight this. The lenders are politically powerful and have plenty of money to buy the low inflation policy they desire.

DeleteWe should raise minimum wage by 10 percent every year until balance sheets recover and demand for goods and services return. Robust wage inflation is necessary for recovery.

I agree with you - though I wouldn't use the term "malefactors." Not everyone who gets rich broke the law or behaved in a socially irresponsible way, per se. (Personally, I think wealth tends to be acquired mostly accidentally, even if the recipients can't admit their happy accidents). Also, not everyone that argues to keep the wealth they have is doing so out of mere personal interest (greed). If we agree that wealth is widely "desirable" then - if our system is to be considered fair - it needs to flow to those that happen to behave most "prudently" (or "guess" right on their investments). That doesn't mean they actually deserve it - they don't. But they do need to get *some* reward else the entire system would have to be deemed capricious - and thus cruel. So once they "earn" it, a progressive tax needs to then encourage them to KEEP earning it (and being productive) else they are no "better" than anyone else.

DeleteAlso, I wouldn't advocate trying to cause inflation via Minimum Wage increases. You should increase the Minimum Wage if it needs to be increased. Period. How much should zero-skill jobs be paid? That's hard to say - but definitely not as much as jobs that do, actually, require SOME basic skills (like reliability, honesty, a strong work-ethic, etc). We do need inflation, true - but we should accomplish that via means that provide a strong reward of higher wages to those with greater skills - because *everyone* is better off whenever *anyone* manages to increase their skills.

All of that said, I am *not* saying the current "system" is "fair" or that everyone's socio-economic place is just-right. There is definitely a lot of unfairness. But the world is not a better place when we demonize anyone who has acquired some wealth or pay everyone a high wage for sweeping floors, etc. We need to be a little more careful in our praise and punishment. Many a good egalitarian socialist found themselves behaving like a bad capitalist once they acquired a little power....

Noah: "During Japan's long deflation, household saving rates fell dramatically."

ReplyDeleteThat doesn't matter. What matters is whether the savings rate was positive (but, also, what the *aggregate* savings rate is - personal, business, and government, minus external trade).

The "dramatic" fall in saving actually happened at the start of Japan's problems - 1997-2001-ish. The reason it fell would tend to be caused by three big factors: changes in the balance of trade and capital flows; changes in the rate of interest offered for savings; and changes in (aggregate) income available to be saved.

The BoJ lowered rates beginning in late 1991 due to economic stress, and they've essentially stayed low since. Meanwhile, the savings rate has been steady since 2001 even though Japan has shifted to a net importer - meaning the actual domestic savings activity has, indeed, increased.

Noah: in response to your final summation...

ReplyDeleteI think it's awkward to talk about how long a recession lasts (with or without a liquidity trap). I think you are confusing yourself by thinking of it that way. Here's why.

An economy is just a big capital flow "system". Some mid-20th century economist (Phillips?) actually created a refrigerator sized economy simulator via water flowing through transparent tanks and regulators. The video's out there if you can find it - it's awesome - his system actually demonstrates long-term cycles that take 10-20 decades to develop in real-life, but 5-15 minutes on the machine.

This is not to say we humans are quite so mechanistic as water molecules (or are we? read: Free Will is an illusion....)

....However, it matters what the cause of a recession is - where did the shock occur? What kind of problem is it? And how big is the problem? Is it a problem that is implicitly fixed (such as a turbulent flow problem? eg: flow instability due to uncertainty in stock markets due to, say, imminent fascist invasion)? Or is it an institutional collapse that has to be repaired? (eg: terrorists nuked the central bank and all the gold reserves?) Or was it a mass "teleportation"/"disintegration" event where the medium of flow (capital/wealth vs water) disappeared or was moved.

The latter describes the shock we had in the Lesser Depression. People and businesses thought they had a certain amount of more or less reliably increasing wealth in real-estate assets, and they leveraged against those assets just like everyone always does. Only in this case, fairly suddenly, that wealth disappeared. It's like a significant chunk of the water in the "consumer assets" tank just disappeared - or, at least, was "teleported" to a "questionable assets" tank and was suddenly out-of-circulation.

That missing medium (ie capital/fluid) means that all the downstream recipients of the flow suddenly experience a massive decrease in flow - and that disruption is slowly propagated through the entire economy. In some cases, the propagation seems instantaneous since humans can see that there's a problem in the suppliers of their suppliers, etc, and they start to take immediate steps (cutbacks) even though the disruption hasn't necessarily hit them yet. But that type of action increases the propagation rate of the flow disruption ("supersonic shock")

What's important is that all of these flow-effects have a significant amount of uncertainty. The initial uncertainty is implicit from the nature of that "asset-value uncertainty tank" the water got teleported to. But by the time the flow disruption (ie: price signal) propogates through the economy, that initial uncertainty causes the margin of uncertainty in almost every other "asset" value to fall into doubt. Even intangible assets. For instance, how safe is Joe Smith's job/income stream? That's a kind of asset whose value-certainty was damaged as the Lesser Depression flow disruption reverberated through the economy. Many incomes fell to zero. Each of *those* events acts like yet another (little) shockwave that must reverberate through the economy. When there are millions of these "micro" reverberations they take the form of a "macro" shock - and cause the value of everything else to take on much more uncertainty - until the reverberation finally dies down *AND* the capital/fluid flow returns to some kind of predictable flow. Even then "normal" will only return when enough people are back to the liquidity-preference that existed before the shock *and* the aggregate asset values (incl. intangibles) are in the ballpark of what it was before the shock, too.

This is easy to grasp when you just think of what happened to people that lived through the Great Depression. My grandparents became ultra-frugal, canned their own food, scorned the taking-on of debt, and they passed that on to their kids - and my wife will tell you that some of that got inculcated into me, too. The point is that some big shocks like this change people - permanently. They cause a marked change in the aggregate preference for debt vs consumption - a change that will only truly go away after 3+ generations via the death of the original generation. And even then, the change will only happen *IF* the economy recovers and leads to a seemingly sustainable and "safe" environment that makes increased leverage seem acceptable to a critical mass of people. (This perceived "cycle" is what leads to the "70-year debt cycle/wave" - but it isn't actually a cycle or wave - it is a chaotic, unpredictable system, dependent on many indeterminate factors...)

DeleteIn short, "recovery" is a bit of an illusion. In some respects, recovery never actually happens. But if you want to know when the economy will get to "full employment," again - it will do so as the reverberations attenuate (which is not a predictable process - the economy is not an echo-chamber - it is more like millions of interacting - *powered* - amplifiers!) and the flow of capital eventually takes on *something like* the flow that previously existed - but (importantly) relative to the new economy. For instance, demographic change means that capital flow patterns (such as tax rates/policies, agricultural/climatic states) will most likely end up in new %-of-gdp values.

In other words, you'll know it when you see it. But that also shows that it is a chaotic system that is not predictable with convenient "less than 5 years" *or* "10-20 year" monikers. In a chaotic system, the more you try to apply a pattern, the more the system will violate the pattern. In the case of a human economy - that violation happens in part because whatever tag you believe applies, there will be others that agree with you - and some number of them will *bank* on that. And those bets will distort the course you'd extrapolated - forcing you to change your prediction. And this doesn't converge into a final, predictable value. Human economies are divergent systems, not convergent systems - because they are always comprised of players whose goal is to exploit the trends, not comply with them. That is the nature of the predictability of chaotic systems.

Noah,

ReplyDelete"Well, some people think that if the central bank is very good at managing expectations... This is what a lot of monetarist blogger types seem to have in mind."

Yeah, I know. Lord almighty!

"Just look at the impulse responses to a policy shock in at Woodford model, dude."

Alright. I see where you are going. But what you said was "In a standard Woodford New Keynesian model, we know how long recessions can be expected to last without policy intervention: maybe about 5 years. In the liquidity-trap models, the characteristic length of a recession without policy intervention is not clear."

That doesn't sound right at all. The right conclusion is that in a (suitably calibrated) basic NK model with no policy response (fixed short rate), or in a liquidity trap we only expect recessions to last 5 (or whatever) years. The "no policy response" and "liquidity trap" models are exactly the same thing, just with a different fixed rate!

"you see econ blogging as sort of an intellectual pissing contest... sometimes you just want to have a conversation with people and figure out what's going on. I guess you can't understand that..."

No, I get it. And you're right. I woke up at 4am, couldn't get back to sleep, read your post and found it muddled. Then took my sleeplessness out on you. I apologize.

Haha no worries. It IS muddled. I haven't carefully worked out a whole macro model since 2009. It used to be that when there was something macro I didn't understand I'd go talk to Miles Kimball or Bob Barsky or one of the grad students. Now I don't have that option so instead I have back-and-forth blog posts with other bloggers... ;-)

DeleteThat doesn't sound right at all. The right conclusion is that in a (suitably calibrated) basic NK model with no policy response (fixed short rate), or in a liquidity trap we only expect recessions to last 5 (or whatever) years. The "no policy response" and "liquidity trap" models are exactly the same thing, just with a different fixed rate!

Yes. That's why it seemed so weird to me that a 20-year deflation could be a standard outcome of a liquidity trap in a NK model.

This comment has been removed by the author.

Delete(Corrected for some typos)

DeleteOk people, you are not listening. It's a liquidity TRAP. The "trap" part means that once you're in it, there's no endogenous, natural mechanism which gets you out of it. The usual adjustment process, flexible prices, is not it, it doesn't work.

You're thinking of it in terms of the standard non-trap model where if output is below potential then prices fall, you move along the downward sloping AD curve, and the economy gets out of recession. But if you're in a liquidity trap falling prices don't adjust anything. They can even make it worse (by moving M/P out to the right where the money demand curve is even flatter) so that whatever traction monetary policy might have originally, it looses it even more.

So, no. It's not muddled. It is not true that "In the liquidity-trap models, the characteristic length of a recession without policy intervention is not clear". It is clear, at least in the bare bones model. Without an increase in inflationary expectations the characteristic length of a recession is "forever".

Of course, per Barkley, it might very well be true that there's other shocks and perks in inflationary expectations get extinguished before anything can happen or that other factors played a role in the particular case of Japan. But as far as theory goes, the model does suggest that a liquidity trap recession can last forever. And yes, you can throw this stuff into a DSGE style model and make it more complicated but at the end of the day it's gonna be just an elaboration on the same basic and simple story.

Am I the only one here who knows how to draw two curves in x-y space that don't cross?

What's interesting is that PK doesn't consider that Japan's somewhat more flexible wages is a possibly contributing reason that it hasn't suffered from tremendously high unemployment.

ReplyDeleteOK now have read half of this post and I'm getting irritated that you didn't respond to my comment below (written after you wrote this post). I disagree with " the mainstream Woodford New Keynesian model and its baby brother the Econ 102 AD-AS model" a baby brother is younger than an older brother. The AS-AD model is almost as old as Woodford and much older than his model.

ReplyDeleteYou identify AS-AD with NK. You say AS-AD does not naturally include a liquidity trap (in fact it does with no problem) because there is only a very first start NK DSGE model with a liqudity trap. The problem here is the interest in "fully worked out" models. Insisting on micro foundations has costs. It implies assuming false things about consumption, investment, the functioning of firms, the existence of marriage (there are competing dynasties which never mix or overlap) the relationship between beliefs and facts (I don't mean the assumption that forecasts are optimal given available information I note that real peoples' beliefs about the recent past are inconsistent with the facts), the nature of investment adjustment costs, the frequency at which prices could be changed if one wished to change it (Gali alarm clock). In exchange for all this there is the great benefit of ... what ?

What of any value would be lost if we decided just to forget all DSGE models and start again with 1960s macro ?

What of any value would be lost if we decided just to forget all DSGE models and start again with 1960s macro ?

DeleteThat is a damn good question, and that was kind of the subtext of my post(s)...

As for AD-AS though, I've never liked it, because the dynamics of the AD curve aren't clear.

Arnott: Mind The (Expectations) Gap

ReplyDeletehttp://www.indexuniverse.com/sections/features/19179-arnott-mind-the-expectations-gap.html?showall=&fullart=1&start=6&utm_source=buffer&utm_campaign=Buffer&utm_content=buffereb7da&utm_medium=twitter

These are complicated matters that can confuse the smartest people, and you did forget about the liquidity trap and there's no shame in that.

ReplyDeleteIf that were true I would readily admit it, since you're right, there is no shame in that. However in this case it happens to be factually false.

DeleteAlthough if liquidity trap models are not that well developed who will pay to fund someone doing research on them. But if they were more readily developed could the return to research on them be higher so could liquidity trap models be in a low investment trap?

ReplyDelete''As for AD-AS though, I've never liked it, because the dynamics of the AD curve aren't clear.''

ReplyDeleteHmm, usually it's the AS curve dynamics that get the flak. Anyway. What would be your go-to example for a short-to-medium term macro model where "the dynamics are clear"?

The Eggertson & Woodford NK model can't really explain a long-lasting liquidity trap. If you adjust the parameters so that the liquidity trap lasts this long (while keeping price rigidity consistent with micro-level evidence), you end up with Mertens & Ravn (2011), where most of the comparative statics are reversed. I think Krugman & Eggertson's debt deleveraging paper is better able to explain long-lasting liquidity traps, but I'm not aware of any actual empirical evidence on that paper.

ReplyDelete"...They also don't (yet) model the effects of supply shocks in a liquidity trap; this is probably relevant for Japan, since its economy experienced a boom in 2002-2006, probably driven by increased trade with China, during which time interest rates and inflation both stayed around zero..."

ReplyDeleteI think one has to be careful drawing conclusions from inflation rates. Based on estimates of potential GDP there's little evidence that Japan experienced a positive aggregate supply shock during the Koizumi Boom. The lack of increase in inflation could simply be due to the fact that the short run AS curve is unusually flat in Japan. On the other hand, since the rate of increase in nominal GDP did go up we know by definition that there was a positive AD shock.

And Japan's nominal imports also boomed during this period so Japan’s net exports only increased from 1.34% of GDP in 2002 to 1.69% of GDP in 2007. Thus net exports added only 0.35% to Japanese GDP during 2003-07, or about 0.07% a year on average:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski2b_7.png

And why did exports boom? Well there's the fact that Japan's real effective exchange rate (REER) fell from 116.25 in February 2001 to 91.09 by March 2006, or by 21.6%:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski2b_1.png

And what caused Japan's REER to fall, and nominal imports to surge at the same time? Could it have been the ryōteki kin’yū kanwa (QE) that was officially announced in March 2001 and which concluded in March 2006? Or are you saying that was purely a coincidence?