How should macroeconomists think about Japan's stagnation? By far the most popular and dominant view of the way macroeconomies work is the monetarist view popularized by Milton Friedman and formalized in DSGE models by Mike Woodford, Greg Mankiw, Guillermo Calvo, Jordi Gali, and other "New Keynesians". This view is so commonplace that many have internalized it.

A quick review for the uninitiated: In this view, the economy's performance consists of short-term "fluctuations" around a long-term "trend". The fluctuations are caused by "demand-side" factors like monetary policy and financial disturbances, while the "trend" is caused by "supply-side" factors like technology, gains from trade, taxes, and institutions.

In the New Keynesian models, which now mostly dominate the core of business cycle research, the demand-side effects come from sticky prices, including sticky wages. (This is not the only way you can get demand-side effects; inattention can get very similar results.) Once the sticky prices have had time to adjust, the economy returns to trend. In most New Keynesian models, the parameter that represents the time that it takes for prices to adjust is the "Calvo parameter". The smaller the Calvo parameter, the longer it takes demand shortfalls to go away on their own. The "short run" is the time during which prices have trouble adjusting; the "long run" is when they've had time to adjust.

In a New Keynesian model, when there is a demand shortfall, unemployment is the result. The central bank can print money in order to combat the shortfall, which raises inflation and lowers unemployment. But if the central bank does nothing, prices will eventually adjust, and unemployment will go away. This New Keynesian model corresponds nicely to the simple AD-AS model that people learn in Econ 102.

Is this kind of model the right way to think about Japan?

At first glance, it would seem that it is. After all, many of the people supporting Abenomics think that expansionary monetary policy will boost the real economy. That naturally suggests a mainstream, New Keynesian model or simple AD-AS model. Here, just for an example, is Nick Rowe thinking about Japan in the context of that sort of model.

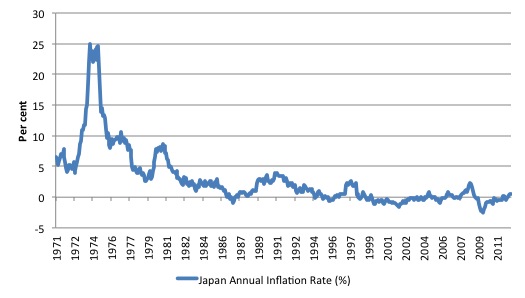

But in order for monetary easing (the "first arrow" of Abenomics) to be the optimal policy in a New Keynesian world, the problem has to be an aggregate demand shortfall. And there are two reasons to think that this may not be what is happening to Japan. First of all, an aggregate demand shock should cause deflation (or disinflation) for only a short time. But Japan's deflation/disinflation has been going on for twenty years straight:

Presumably, prices and wages are able to adjust in 20 years' time. So an aggregate demand shock, even one as big as the bursting of the Japanese bubble in 1990, should not last nearly this long.

And there is the question of whether Japanese wages and prices are even particularly sticky in the first place. Here are Japanese wages:

Wage growth is sharply negative in some years, indicating that Japanese wages may not be so sticky. See also here. (Compare this to the U.S., where wages failed to fall much even during the big recent recession.)

{kind=link}

So how can we be looking at a sticky-price story for Japan's stagnation? Well, we could be looking at a very long series of negative demand shocks. Japan could have just kept getting hit with shock after shock, giving the appearance of a long steady decline. But what were those shocks? If they were global in nature (such as the Asian financial crisis, the tech bubble, etc.), there's the question of why other countries around the world haven't mirrored Japan's deflationary experience. And a long string of negative domestic demand shocks is not in evidence.

It seems to me that the standard New Keynesian sticky-price story just cannot explain Japan. The "short run" for Japan is over and done. We are not looking at a "short-run" fluctuation caused by sticky prices.

This has implications for policy. It means that we can't expect the "first arrow" of Abenomics - quantitative easing - to boost the real economy through the kind of channel described by a New Keynesian or AD-AS model. It might do so through some other channel, but how exactly that will work is not clear.

What about the supply-side? Is Japan living in an RBC world? Well, it's true that Japan's total factor productivity has flatlined since the early 90s. Here's a not-quite-up-to-date graph from Hoshi & Kashyap (2011), but recent years have not looked any better:

This could suggest an RBC-style story of institutions and regulation choking off productivity growth (which is, in fact, the story Hoshi and Kashyap tell).

Also, Japan's labor hours per employed person have been in secular decline for about the same amount of time:

This suggests that Japan's stagnation could be partly caused by people deciding to work less - not necessarily a bad thing in a nation infamous for overwork. Instead of a "great vacation", call it a "great coffee break".

But I don't think Japan is living in an RBC world either. Because in an RBC world, keeping interest rates at zero for decades, and printing a bunch of money (as the Bank of Japan did in the mid-2000s), should cause inflation (without helping growth). Instead, we see persistent deflation. So an RBC model of the common type can't be describing Japan's world either.

So what sort of model is Japan living in? I'm not sure I know any model that describes Japan; maybe we don't have one. But my guess is that it's a world in which "Aggregate Demand" and "Aggregate Supply" are not as distinct entities as they are in Econ 102. In an AD-AS framework, either the AD curve or one of the AS curves shifts on its own. But in Japan, it may be that what look like supply shocks (falling productivity) and what look like demand shocks (deflation) may actually be due to the same cause.

And whatever world Japan is living in may have multiple equilibria. It may be that Japan is trapped in a "bad equilibrium", and it will require a "big push" to kick it back to the "good equilibrium". In fact, that seems to me to be the implicit premise of Abenomics.

In any case, we shouldn't be thinking about Japan solely in terms of our standard textbook models. The real world appears to be much weirder than those toy environments.

Update: Paul Krugman says zombies have eaten my brain:

Yes, in a standard AS-AD or NK model, high unemployment leads to falling wages and prices, and this eventually restores full employment...

[But]the only reason deflation “works” in the standard model is that it increases the real money supply, which leads to lower interest rates; in effect, it acts like an expansionary monetary policy...

But Japan has been in a liquidity trap during the whole period Smith looks at. Monetary expansion is ineffective unless it can raise expectations of future inflation. Deflation is definitely not going to help. In fact, by raising the real burden of debt, it makes things worse...

A corollary is that while sticky wages are a real phenomenon...They are not, repeat NOT the reason either Japan or we have failed to recover.But this doesn't really contradict what I was saying in this post. Just like Krugman says, a standard AD-AS or New Keynesian model would imply that Japan's deflation would have gone away on its own long before now. That was my point. So I'm not sure zombies have eaten my brain. (Then again, with no brain left, how is one to know?)

Now let's talk about liquidity-trap models. The story that Krugman tells - debt-deflation keeping price adjustments from clearing markets - is intuitively plausible (to me, anyway). I freely admit that I have not worked through a liquidity trap model in sufficient detail to know all the ins and outs of how one works. In one of these models - for example, Eggertson & Krugman (2011) - are there multiple equilibria? Is it possible for a negative shock to push a country into a bad liquidity-trap equilibrium, out of which it cannot escape unless it receives a big "kick" (from policy or from a positive exogenous shock)?

If so, then liquidity-trap models of the Krugman type are a candidate for the "multiple equilibria" story that I said I think is necessary in order to explain Japan's stagnation as a demand-side phenomenon. If liquidity-trap models are the replacement we need for textbook AD-AS and New Keynesian models, then economists and the general public need to thoroughly revise the intuition that we use to think about recessions.

But if liquidity-trap models do not contain multiple stable equilibria, then the length of Japan's deflation needs a different explanation. Frighteningly, the answer may depend on whether the model is linearized or not. (Note: It would also be easier to answer if I could find a set of impulse response graphs for a liquidity-trap model. But I can't find one...)

(Note that though I haven't worked through the details of an Eggertsson-Krugman type model, I do know other modified New Keynesian models that include a "bad equilibrium". One of these is a model by Miles Kimball and Bob Barsky, which they have not yet published online as a working paper. They should get around to doing that!)

Update 2: Ikeda Nobuo, Japan's most widely read econ blogger, responds (in Japanese), attributing Japan's stagnation to a long-term sectoral shift. Shades of Joe Stiglitz.

Update 3: Steve Williamson chimes in, chiding me for equating AD-AS with a standard New Keynesian model, and discussing liquidity traps with some simple graphs.

I can't find the evidence for it now, but anecdotally isn't there a fair bit of government involvement in the private sector - supporting zombie companies that would otherwise have gone bust under a classical model - lemon socialism I think some call it...?

ReplyDeleteThinking of this?

Delete"Zombie Lending and Depressed Restructuring in Japan"

http://dornsife.usc.edu/IEPR/Events/Papers/Anil_Kashyap.pdf

Yes!

ReplyDeleteJapan is very interesting. Flat productivity and declining working hours can also be a sign of inadequate demand.

What you need to look at here is what is happening to the velocity of different definitions of money. I suspect an aging population desperately trying to maintain their savings, is killing the velocity of circulation. You need to give more money to younger people to get things going again.

Finally someone gets the demographic disaster magnified by idiotic employment policies.

DeleteIn short, no jobs for youth, and an aging workforce grimly clinging to their crappy jobs.

No huge growth driven by poor family formation, driven by the lack of jobs.

I guess the folks sitting at home in their parent's basement here should shut off the Xbox long enough to worry about the future, or tell the gummint to sufficiently stimulate employment for all of those college grads hiding from the real world.

Zonker eventually had to graduate, and I imagine the shock for all of them hustling for yet another barista gig will be immense.

Aggregate demand here is declining in tandem with our boomer aging demographic, and yet we think all is well.

Japan is our future.

>>Japan is our future.

DeleteDoes that include national health insurance?

From Wikipedia

Deletehttp://en.wikipedia.org/wiki/Health_care_system_in_Japan

"The health care system in Japan provides healthcare services, including screening examinations, prenatal care and infectious disease control, with the patient accepting responsibility for 30% of these costs while the government pays the remaining 70%. Payment for personal medical services is offered through a universal health care insurance system that provides relative equality of access, with fees set by a government committee. People without insurance through employers can participate in a national health insurance programme administered by local governments. Patients are free to select physicians or facilities of their choice and cannot be denied coverage. Hospitals, by law, must be run as non-profit and be managed by physicians. For-profit corporations are not allowed to own or operate hospitals. Clinics must be owned and operated by physicians."

But this just means that the Japanese have to give up on having the superior outcomes that we have here in the for-profit, market based healthcare system. Or at least that's what my Louie Gomert and Steve King told me.

But wait.

"People in Japan have the longest life expectancy at birth of those in any country in the world. Life expectancy at birth was 83 years in 2009 (male 79.6, and female 86.4 years respectively)."

"People in Japan have the longest life expectancy at birth of those in any country in the world. Life expectancy at birth was 83 years in 2009 (male 79.6, and female 86.4 years respectively)."

DeleteMight want to dis-aggregate life expectancy by various demographic groups (of which Japan has more or less...one) before assuming that Japan has a vast advantage here.

Be sure to include the 10 million plus US residents recently imported (from a neighboring lower health nation) by a certain political party in order to increase said party's political power.

I've only read your first two paragraphs and I'm already wanting to disagree with you.

ReplyDelete1st paragraph. Monetarism is not the same as New Keynesianism. In fact, I'm pretty sure you know that, so I'll just assume you bundled them together for the sake of brevity and to irritate pedants like me.

2nd paragraph. Huh? What? No! There are plenty of supply-side shocks in a standard New Keynesian model. In fact, in every DSGE I've ever encountered, *most* shocks are on the supply side. Only monetary policy shocks are unequivocally on the demand side. Even the good 'ol fashioned shock to the utility of consumption has supply-side elements to it, since it affects the household labour supply and hence (through real wages) firms' marginal costs.

Monetarism is not the same as New Keynesianism. In fact, I'm pretty sure you know that, so I'll just assume you bundled them together for the sake of brevity and to irritate pedants like me.

DeleteHaha TROLLED. Also NK = monetarism, tis true.

There are plenty of supply-side shocks in a standard New Keynesian model. In fact, in every DSGE I've ever encountered, *most* shocks are on the supply side. Only monetary policy shocks are unequivocally on the demand side. Even the good 'ol fashioned shock to the utility of consumption has supply-side elements to it, since it affects the household labour supply and hence (through real wages) firms' marginal costs.

A) Sure there are negative supply shocks but they don't tend to lead to deflation.

B) Supply shocks are quantitatively small relative to demand shocks when NK models are estimated.

C) The effect of the shocks should still last a lot shorter than 20 years.

This reminds me of something that Andy Harless once said.

DeleteThe old dispute between the Monetarists and the Keynesians was resolved when the Keynesians conceded all the substantive points and the Monetarists agreed to be called New Keynesians.

That is an heresy, Monetarists aren't Keynesians, they use a derived Keynesian model, but philosophically they aren't Keynesians.

DeleteActually I have a big problem with the so called NK, if they don't acknowledge that full-employment isn't the "de facto" situation but only a possible equilibrium point, they are violating the core of the Keynesian theory. They should call themselves Classic or Neo-Classic

(But I do like the rest of your post)

ReplyDeletehehe thanks

DeleteIf we line up Japan demographics and Japanese inflation, don't they pretty much line up? Inflation in the 1960s and 1970s, during the demographic bubble, deflation in the 1990s and 2000s, coinciding with demographic decline. Old people just don't go out and buy houses, cars, furniture and electronics, no matter what the monetary policy.

ReplyDeleteNeither do some young people: http://en.wikipedia.org/wiki/Hikikomori

DeleteCouldn't Japan just be a function of flatlining and aging population and that's it? Who says aggregate demand always has to increase?

ReplyDeleteNoah - you a contemplating all the right questions and coming up with the correct conclusion that Japan requires a distinct analysis. But that analysis may not be as complicated as you think (or unique, because I think it applicable to the advanced world at large in recent years).

ReplyDeleteJapan's debt deflation began (arguably in 1992 - when lending finally stopped after the 12/89 crash) only a couple of years prior to the Asian Tigers hitting their stride and materially undercutting Japanese export pricing with high-quality "mid-value-added" exports that were Japan's sweet spot. Japan's wages and prices had to fall of course, and did.

After Koizumi and Takanaka finally confronted the debt overhang in 2002, we were well along with the emergence of the BRICs as massive export and surplus economies....causing more downward pressure on Japanese prices and wages.

Of course, declining prices also have the effect of supporting one's currency if you make stuff that people outside the country want to buy. So in recent years, Japan has faced the double whammy of a strong Yen - to some extent merely because the ¥'s purchasing power has increased internally.

All of this is outlined in a section of my upcoming book, "The Age of Oversupply" to be released by Penguin in September.

Regards,

Dan Alpert

Fitting title I can't wait to read..promote it well so I do not miss it! ;0)

DeleteWhat does it mean for a central bank to "do nothing"? I would say that as long as the CB exists, it must be doing something (which is not to say it must be transacting in financial markets).

ReplyDeleteIf you break the data in terms of just working age pop. the issues don't look nearly as severe...pointing to it being mostly a demographic problem?

ReplyDeleteThe productivity shown is total factor productivity, not labor productivity. So that's not an issue here.

DeleteBut I don't think Japan is living in an RBC world either. Because in an RBC world, keeping interest rates at zero for decades, and printing a bunch of money (as the Bank of Japan did in the mid-2000s), should cause inflation (without helping growth).

ReplyDeleteWhat if they just buy long-term financial assets with the money?

Japanese household savings rates fell to near zero over the years. That speaks to low labor liquidity.

ReplyDeletehttp://www.oftwominds.com/photos10/japan-savings7-10.png

Unit labor costs, which are labor's share of income times the price level, tracked down with the retail trade.

http://research.stlouisfed.org/fredgraph.png?g=kBr

Capacity utilization has been tracking downward in Japan, which to me represents a decline of labor's share of income.

http://www.tradingeconomics.com/charts/japan-capacity-utilization.png?s=japancaputi&d1=19680101&d2=20130531

And then labor income share (LIS) itself has declined over the years.

http://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CDIQFjAA&url=http%3A%2F%2Fwww.iza.org%2Fconference_files%2FESSLE2010%2Fagnese_p5029.pdf&ei=8BPkUfeACqOEiAL0mYGIBg&usg=AFQjCNFSa8eNAgcQFZEqQRFjBMfCVvrbzA&sig2=eyEY_qalNL_HVgzYxurUVg&bvm=bv.48705608,d.cGE

If you look for another model to explain Japan, it would be good to look for one that incorporates labor's share of income... labor's relative power to consume.

I like the last link. But I certainly wouldn't ignore demographics on top.

DeleteSticky wages/prices? Tsk. Always seemed like such a waste of a decent premise (AD matters); for my own take on sticky wages:

http://theredbanker.blogspot.fr/2013/03/sticky-wages-i-dont-think-so.html

and, for my own take on Japan's printing:

http://theredbanker.blogspot.fr/2013/06/on-scott-sumner-monetary-policy.html

Wow, this post is one huge piece of Krugman-bait. Will be interesting to see what he has to say.

ReplyDeleteYou can read it for yourself right here:

Deletehttp://krugman.blogs.nytimes.com/2013/07/15/wage-price-flexibility-in-a-liquidity-trap-again-again-again/

I was right. It is interesting.

DeleteWhat is your definition of "stagnation"? Can I see comparative age-weighted per-capita GDP growth statistics against other developed countries, along with more research into the motivations of employed persons regarding their preferences for longer or shorter working hours?

ReplyDeleteThat'd be helpful. Thanks.

I think you're mistakenly assuming that if it has to do with aggregate demand then it has to be the result of 'shocks', which are by their nature temporary. Keynes feared that the long-run norm would be that desired savings would be higher than desired investment at full employment, even at zero nominal interest rates - that is, a chronic liquidity trap. I think is also Krugman's view of Japan.

ReplyDeleteKeynes's answer was to socialize investment to keep it high enough to maintain full employment. Krugman's answer is higher inflation and a correspondingly more-negative real interest rate.

So this is a straight-forward model - IS-LM, or IS-PC-MR, etc. - that seems to explain it. I don't know if this long-run outcome can be micro-founded using the standard preferences and optimizing behaviour of the New Keynesian framework (even Eggertsson and Krugman is still a short-term model). But if not, all the more reason to prefer the reduced form IS-PC-MR to the full micro-founded version.

You seem to be making this far more complicated than it is.

ReplyDeletePart of the title of your post is "demand side or supply side?" The answer to the question is yes (it is indeed both). The the good old simple AD-AS model is indeed the way to think about it:

http://2.bp.blogspot.com/_b6CLevEGCD0/S6E-XRrJo8I/AAAAAAAABtI/tHf8xEgh6Ao/s1600-h/ADAS.jpg

How do we measure aggregate demand (AD) in practical terms? With nominal GDP (NGDP) of course. The five year average growth rates of NGDP were 6.4% in 1985-90, 2.2% in 1990-95, 0.2% in 2000-05 and -0.9% in 2005-10. So there has been a decrease in the rate of increase in AD.

How do we measure aggregate supply (AS) in practical terms? With potential real GDP (RGDP) of course. The OECD's estimates of Japan's potential GDP show that the five year average growth rates of potential RGDP were 3.0% in 1985-90, 2.4% in 1990-95, 1.3% in 1995-2000, 0.7% in 2000-2005 and 0.6% in 2005-10. So there has been a decrease in the rate of increase of AS.

Now, if you want to figure out why the growth rates of AD and AS each have slown down, or perhaps how one has impacted the other, then that is the subject of two, or perhaps three or four more posts.

Correction:

DeleteNGDP decreased at an average rate of -0.2% in 2000-05.

Omission:

DeleteNGDP decreased at an average rate of 0.3% in 1995-2000.

Correction of Omission:

DeleteNGDP *increased* at an average rate of 0.3% in 1995-2000.

(I'm completely cognizant of the fact this is irrelevant. This is purely for my sake.)

Didn't the BoJ raise rates in 2000 and 2006 and don't those count as demand shocks?

ReplyDeleteDemographics are not temporary and affects both supply and demand. Japan may be on the leading edge but Europe and China aren't far behind and even we will face deflationary pressures as we age.

ReplyDeleteShame, this analysis ignores the inconvenient truth staring everyone in the face.

ReplyDeleteEconomies with a LR declining population can't adopt a system that requires a perpetual-growth output (or debt-based monetary system).

Japan will never default on its external debt, and Japan will never have hyperinflation, and it will never have "normal" rates ever again. The sooner everyone accepts this, the better. It's got a declining population, and there's no way that productivity, exports, inflows would ever make up the difference needed to produce the rates of growth that facilitate the non-ZIRP environment needed in a debt-based perpetual-growth paradigm. Barring some major reformation that leads to an acceptance of immigrants or huge birth rates, the Japanese economy will continue on the way it has for decades -- flat, rich, and predictable.

You're welcome.

Declining and aging populations are no impediment to the generation of inflation provided you have a determined central bank. Take Belarus, Hungary and Russia for example. Belarus had nearly 60% inflation last year.

DeleteThose are developing nations. They're separate from the effect on developed economies who suffer from the stagnation.

DeleteDeveloping nations can have declining nominal population, but have the effect of an increasing labor force that can prop up industrial growth where development is lacking.

You can generate inflation by spending prolifically or with foreign-currency-denominated external debt, as in Belarus and Hungary (swiss franc loans), respectively.

But Japan has developed, and they are too cautious to engage in the spending that would generate inflation, and it wouldn't generate real growth anyway because there's no more room for it for them.

So, what I mean is that Japan doesn't have the capacity to produce that growth that would bring along with it modest inflation...until the demographics are addressed by a radical cultural change.

"Developing nations can have declining nominal population, but have the effect of an increasing labor force that can prop up industrial growth where development is lacking."

DeleteI am unable to verify this through a database, but I've read in a number of places that the labor force in both Russia and Belarus is declining even faster than the population as a whole. And according to the the European Commission's AMECO database Japan's labor force increased last year and is forecast to do so again this year. Hungary's labor force declined from 2006 to 2009 but has increased since.

More importantly, Hungary is classified by the UN as posessing a "very high human development" (in the top category with Japan) and Belarus and Russia are classified as posessing "high human development". So just how developed does a country have to be before declining population guarantees deflation?

"You can generate inflation by spending prolifically or with foreign-currency-denominated external debt, as in Belarus and Hungary (swiss franc loans), respectively."

And Russia is net creditor having run a current account surplus for many years. Nevertheless it had double digit inflation as recently as 2005 and had over 5% inflation last year.

Aside from the false assertion that the Russian and Belarus labor forces are declining faster than the population (it's not true, IndexMundi, TradingEcon all have international databases that you can confirm it on). What I said specifically was the _effect_ of a higher labor force. When developing, a nation has more slack to generate growth from investment, so theoretically even if the population is dropping, there's so much "development slack" that it carries what would otherwise be negative growth into positive territory.

DeleteHungary is not on the same development level of Japan, that's just silly (it's not even half as wealthy in GDP). Japan is a legitimately wealthy nation, Russia/Hungary/Belarus are absolutely not (yet developing and with lots of potential)

And Hungary's inflation was/is due to the foreign-currency-denominated debt load they had, largely in Swiss Francs, which when chased, led to domestic-currency price inflation.

Russia has been hemmorrhaging FX reseves and they can maintain growth rates that pull inflation because they've had major structural reform in the past decades. And they can force surpluses and growth through natural resource extraction, which Japan doesn't have the same luxury.

Japan had this amazing period in the 80's which involved high growth, healthy inflation as a result, etc. They built up a wealth level that has been maintained as their demographic situation has come to a head. It's over now. They're stuck where they are, which, considering they're one of the richest and most admired economies/cultures in the world, is not too shabby.

So focus on the bigger picture and hard data, not meaningless UN classifications. When in the period of development classified by high investment and higher growth rates, this can masque structural issues that add deflationary pressures.

And the solution? It's to re-envision debt money and perpetual growth for developed rich countries like Japan. Some have abundant natural resources that deliver growth that covers demographic issues, like Russia. Some are in periods of development that deliver higher growth that mask the same issues. And others, like Japan, need to figure out some way to eliminate all that debt without eliminating all that money. Which when you think about it, is incredibly simple, if there's courage and appetite for radical systemic change.

"Aside from the false assertion that the Russian and Belarus labor forces are declining faster than the population (it's not true, IndexMundi, TradingEcon all have international databases that you can confirm it on)."

DeleteFrankly, Indexmundi and TradingEcon are terrible sources for data. According to the World Bank Belarus had a declining labor force from at least 1990 until 2009. Furthermore the labor force to population ratio declined throughout that period:

http://data.worldbank.org/indicator/SL.TLF.TOTL.IN

Furthermore the IMF projects that it will continue to decline in the future:

http://www.imf.org/external/pubs/ft/scr/2012/cr12114.pdf

The labor force of Russia declined from at least 1990 through 1998 during which time it declined faster than the population of Russia. It has increased since then but it remains below the level it was in 1990 and is projected by the World bank to decline between now through at least the 2020s (page 8):

http://siteresources.worldbank.org/INTECA/Resources/RussiaGrowthAccountingLaborJuly122011).pdf

"What I said specifically was the _effect_ of a higher labor force. When developing, a nation has more slack to generate growth from investment, so theoretically even if the population is dropping, there's so much "development slack" that it carries what would otherwise be negative growth into positive territory."

This is totally incoherent. What is the source of this "development slack"? The word slack usually imples some unused factor of production (labor or capital). But you are talking about "investment" which implies the creation of new physical capital which is not the same as increasing production by employing unused capital.

"Hungary is not on the same development level of Japan, that's just silly (it's not even half as wealthy in GDP). Japan is a legitimately wealthy nation, Russia/Hungary/Belarus are absolutely not (yet developing and with lots of potential)"

According to the IMF the GDP per capita of Hungary and Russia is about two thirds that of Japan when adjusted for PPP:

http://stats.oecd.org/index.aspx?queryid=558

And Japan's GDP per capita in turn is only about two thirds of the US. So where is this mysterious cutoff that grants a nation developed status according to your own private idiosyncratic definition?

"Russia has been hemmorrhaging FX reseves and they can maintain growth rates that pull inflation because they've had major structural reform in the past decades. And they can force surpluses and growth through natural resource extraction, which Japan doesn't have the same luxury."

There was a large drawdown in Russia's foreign exchange reserves from July 2008 to March 2009 during the global financial crisis when they fell from $596 billion to $384 billion:

http://www.imf.org/external/np/sta/ir/IRProcessWeb/data/rus/eng/currus.htm

But they were back up to $538 billion as recently as December and are $518 billion as of May and are the fifth largest in the world after China, Japan, Saudi Arabia and Switzerland:

http://en.wikipedia.org/wiki/List_of_countries_by_foreign-exchange_reserves

"So focus on the bigger picture and hard data, not meaningless UN classifications."

The UN classifications refer to "economic development". Economic development is a broad concept that is not the same as GDP per capita. It also takes into account health and education for example. GDP per capita *is* the the small picture.

http://en.wikipedia.org/wiki/Economic_development

Furthermore you are throwing in all sorts of ridiculously distracting minutiae (labor force versus population distinction, net international asset positions, foreign reserves, etc.). And you are evidently claiming that Japan's deflation is the combination of a shrinking population and its GDP having attained some mysterious minimum level which you have still yet to define.

This may as good a post as any to debut something I've been working on for a year or so. (It's never been hit by outside comments so go easy on me.)

ReplyDeleteI put together a basic supply and demand framework based on information theory and then implemented a quantity theory of money in that framework. It has elements of an AD-AS model but AD and AS are strongly coupled (as Noah hints at above).

This is a set of links I put together for an overview:

http://informationtransfereconomics.blogspot.com/2013/07/short-course-on-information-tranfer-and.html

But the interesting thing is that is does pretty well at describing Japan as a persistently deflationary environment since the 1990s even though the money supply is increasing.

http://informationtransfereconomics.blogspot.com/2013/07/a-more-global-perspective.html

The problem is that the ratio of the base to GDP has gotten to large which changes the model behavior from a traditional quantity theory into something quite different. The unfortunate thing is that this model also says the US has recently entered the exact same territory.

(n.b. I'm not some sort of hard money gold bug; I am in favor printing money as a tool of demand management.)

My guess is that Japan is still suffering from the big tax cuts they put in after the boom years of the 80s which were noted for their outrageous marginal tax rates. (The A Taxing Woman movies were part of this. People were actually abandoning money in empty lots to avoid paying taxes on them.)

ReplyDeleteThe problem with interest rates is that high interest rates actually can stop borrowing, but low interest rates cannot induce it. It is asymmetric. This means that high rates can cut demand, but low rates cannot increase it. Monetary policy is basically a one way ratchet screwdriver.

Japan, like most of the developed world, suffers from flat wages and too high a savings rate, both symptoms of income inequality. Japan needs to figure out excuses that let it take money from savers and give it to people to spend, rather than save. Poorer people spend more of their incomes than richer people, so you'd want to give it to poorer people, and there are plenty of poorer people in Japan, old and young.

PK responded: http://krugman.blogs.nytimes.com/2013/07/15/wage-price-flexibility-in-a-liquidity-trap-again-again-again/

ReplyDeleteReply or update forthcoming Noah?

Makes popcorn ...

DeleteI supersized - this should be good!!!

ReplyDeleteEconomics is one of those subjects where two people can argue about something and neither is right.

ReplyDeleteTrue of pretty much every subject ...

Deleteand neither is even wrong!

DeleteJapan grew by exporting more and more manufactured goods to the West. With the low hanging fruit picked, and China, Taiwan and Korea competing with them it was no real mystery that Japan stagnated. Add in inflated gdp numbers based on mis-pricing of real estate and the picture may be complete.

ReplyDeleteAnd whatever world Japan is living in may have multiple equilibria.

Japan is a trading economy (with a floating exchange rate) in a much larger global economy. If there are multiple equilbria it is only because each set of policy choices will give rise to a different equilibrium. Pick your policy set and the equilibrium will be set - although it may take decades for the economy to move to a new equilibrium.

I think you make a good point on the medium and long term Japanese problem. I am looking forward to Noah's response to the Shrill One. Generally, at least the last six years, I have found with one exception that Brad Delong's two rules of Paul Krugman govern such discussions. 1) Paul Krugman is always right and 2) If you disagree with Paul Krugman, remember Rule No. 1. The exceptioin is where Dean Baker disagrees with Paul Krugman, which is seldom, but then Dean is always right. http://www.cepr.net/index.php/beat-the-press/

DeleteHmmm, ad hominem attacks. Insecure much?

DeleteI think you are right. Japan's unemployment is around 4%, near the natural level. Deflation is the result of lower wages, as you showed. So it is stagnant at near the potential output.

ReplyDeleteThe problem is the low TFP especially in the non-manufacturing sectors. Japan is a two-sector economy, as I explained in my blog (in Japanese).

http://ikedanobuo.livedoor.biz/archives/51864624.html

This seems intuitive, but how does it explain the deflation?

Delete"So it is stagnant at near the potential output."

DeleteThe BOJ’s own estimates of the output gap put it at about 4% of potential GDP in 2011Q2 (Figure 9):

http://www.boj.or.jp/en/research/wps_rev/wps_2012/data/wp12e06.pdf

Deflation is explained by the LACK of wage rigidity in Japan.

ReplyDeletehttp://livedoor.blogimg.jp/ikeda_nobuo/imgs/6/4/64b7c063-s.jpg

The level of potential output is controversial in Japan. OECD estimates that there is no output gap in Japan.

http://ikedanobuo.livedoor.biz/archives/51861165.html

Great Post...Thank you very much ...

ReplyDeleteGreat post. Japans' predicament can be explained reasonably well by a neo-Wicksellian model which compares the natural and money rates of interest. During the 1990's, its cost of capital (money rate) remained higher than its return on capital (natural rate) causing capital destruction. This was partially driven by the fact that Japanese companies did not default as they should have done but were kept alive by the banking sector (read government). This is why the CDS market in Japan traded around 1/3 the level of the US market. The return on capital in Japan is now positive and rising but at a level 50% lower than the US. Until that rises, it is unlikely that Japan will generate much more sustained growth. See link for a comparison of natural rates. The data also demonstrates why the UK is still suffering compared to the US (driven by the poor performance of its banking sector)

ReplyDeletehttp://www.creditcapitaladvisory.com/2013/02/13/2013-asset-allocation-a-credit-based-disequilibrium-approach/

I don't think you can look at the full 20 years as a whole and look for a single explanation. The first 5 years following the asset bubble was really just reluctance by the banks to publicly acknowledge the high level of non-performing loans on their books; which was enabled by poor corporate governance (only 35% of banks had outside board members). The government was also slow to react, which only perpetuated the problem. So 10 years in, you finally have banks and governments taking appropriate measures to rectify the situation. The sticky wages was merely a spillover effect. Another large issue that doesn't get much attention is Japan's "lost generation": those workers pessimism about the future grew as stagnation continued. One might look at the lower working hours as "finally the Japanese worker is taking it easy" when it reality it shows the lack of vitality that their elders had during the boom leading up to the 80's. The uncertain consumer pulled back the reins and savings increased throughout the 90's, leaving companies with growing inventories, falling prices, and deflation.

ReplyDeleteSo on paper, 20 years seems like a long time, but in reality 2002-2006 is probably the most mysterious time of the stagnation.

“There are four kinds of countries: developed countries, underdeveloped countries, Japan, and Argentina.” – Simon Kuznets (apocryphal)

ReplyDeleteI agree that price stickiness must long since be over. After all, Japan's unemployment is far lower than other developed countries. As Eli Dourado says, the short run is short. I think demographics play a larger role than most people think.

I think the disagreement is because Paul Krugman is using a different New Keynesian model. If you are interested, I elaborated more on that here: http://hyperplanes.blogspot.com/2013/07/a-tale-of-two-new-keynesian-models-or.html

ReplyDeleteI'm nowhere near qualified to judge these issues, but Matthew Martin's linked explanation is remarkably lucid. I recommend it to other interested but confused laypersons.

DeleteYup. This is good, thanks Matthew.

DeleteWell now I've read it. I feared I wouldn't like this post. Then Krugman said zombies ate your brain and I thought I knew what the source of your disagreement was. But I had to read the post to know. I must say it won't give me nightmares. I disagree with roughtly 4 letters and a hyphen AS-AD. The point where you and I disagree is "This New Keynesian model corresponds nicely to the simple AD-AS model that people learn in Econ 102." I think this is not true at all. I think the Japanese case shows the not general validity of New Keynesian models. However, it doesn't show any problem with economics 102 AD-AS models.

ReplyDeleteIn particular, it is no problem for an IS-LM model (it better not be as Keynes and Hicks were considering a long lasting depression). The LM curve gives increasing nominal interest i as a function of GDP Y. It is horizontal at i=0 (the liquidity trap). The IS curve gives i as a decreasing function of Y. If it shifts far enough left then they cross at i =0 and Y low and unemployment higher than the NAIRU. In this case inflation falls and falls. In the USA it appears alll the way down to 1%/year and in Japan down to actual deflation.

There is, as Krugman notes, no problem at all in including the case of Japan in an IS-LM-Phillips curve model.

In contrast, the data are absolutely inconsistent with standard modern NK models.

What went wrong ? Well just for simplicity standard NK models have utility functions such that the demand for real balances can't be satiated (additively separable in consumption leisure and real balances and CES in each). This means that a liquidity trap is impossible in modern NK models. The models are clearly fundamentally false and grossly misleading. In contrast, the IS-LM-Phillips curve model appears to be a useful approximation.

It definitely can have a horrible equilibrium with hyper deflation. It definitely can have a bad equilibrium with permanent depression unless and until there is fiscal stimulus. This depends on the shape of the Phillips curve and the position of the IS curve. Now this may just show that if one is ad hoc enough one can fit anything and explain nothing. But it is bettr than a fancy model which proves that the cases of Japan and the USA 29-32 are impossible.

Haha sorry for not responding earlier, you must realize I'm on the other side of the world... ;-)

DeleteAD-AS can of course describe most any macroeconomic phenomena as long as you get to choose the shape of the curves and make any assumptions you like about which curve shifts and when. That's just called "plotting a point on a Cartesian plane and labeling it". So in that sense, AD-AS can "explain" anything.

But the way it gets taught in Econ 102 (by me, and by the profs I worked for), with an AD curve that slopes down everywhere, curves that shift independently, and an SRAS curve that adjusts within a few years, cannot explain Japan. That is what I meant.

Eight years ago we proposed a model (http://ideas.repec.org/p/nos/tttehw/mechonomics6.html) showing that inflation would not visit Japan till 2050. We checked (http://ideas.repec.org/p/arx/papers/1002.0277.html) the result in 2010 and found no deviation in the future: deflation -1% per year. Unemployment will be hovering around 5% in the years to come. Both macro variables are driven by decreasing working age population. In the long run, GDP per capita should grow 1% to 2% per year.

ReplyDeleteScott Sumner would say (I think) that it wasn't a demand shock, it was a change in the monetary policy rule. The BoJ shifted its inflation target to about zero. On the wage graph, you can see before 2001 and 2006 wage growth peeks above zero. Both times the BoJ took explicit action to tighten policy and push it back down.

ReplyDeleteIn light of the experience of the last few years, it seems pretty likely that the New Keynesian assumption of symmetric nominal rigidity is wrong. If instead there's some kind of especially sticky stickiness around zero, then could a quasi-depression (which for them I guess means unemployment above 3%) caused by persistently tight money be an equilibrium?

I like this 2011 Tyler Cowen post:

ReplyDeletehttp://marginalrevolution.com/marginalrevolution/2011/08/how-bad-is-it-in-japan.html

I think it might help if when talking about Japan's stagnation, people defined exactly what they mean by stagnation.

One question that's relevant here (and I apologize if this is covered elsewhere; I'm not that frequent a reader, nor am I super immersed in the theory) is why TFP is considered a 'supply side' phenomenon? In the Equation Y = AK^bL^(b-1), why does Y have to represent GDP and not GNE (earnings that people actually get to take home)? It is equally viable IMO to say that economic growth comes from technological advancements, as the ability to apply those technological developments towards practical needs with real demand. Anyone in marketing knows their role is to create demand - and marketing is where a good portion of innovation comes from. This area is also where I see Asian economies struggling the most.

ReplyDelete